What Is a Term Sheet? Understanding Investment Agreements in Pakistan

⚡ Quick Answer: A term sheet is a non-binding summary of the key financial and legal terms that an investor (like a Shark on Shark Tank Pakistan) proposes before signing a final investment agreement. For a term sheet Pakistan startup founders encounter, it outlines the valuation, equity stake, investor rights, and conditions—but crucially, most of it is not legally enforceable in Pakistani courts except for specific clauses like confidentiality and exclusivity.

You have just walked out of a pitch meeting. A Karachi-based venture fund or perhaps a Shark from Shark Tank Pakistan has shown genuine interest. The email lands in your inbox with the subject line: “Term Sheet Attached.” Your pulse quickens. Excitement. Then confusion. What exactly are you looking at? Is this a binding contract? Should you sign it immediately? And what do all these clauses—liquidation preference, anti-dilution, drag-along rights—actually mean for your Lahore-based SaaS company or your Faisalabad textile startup?

If you are a Pakistani founder navigating early-stage funding, understanding the anatomy of a term sheet is not optional. It is the single most important document you will review before money hits your account—and yet, most founders spend more time polishing their pitch deck than learning how to read one. This guide changes that. Written specifically for the Pakistani startup ecosystem, it covers everything from the binding vs non-binding nature of term sheets under Pakistani law to how Sharks on Shark Tank Pakistan structure their on-air offers.

Why Every Pakistani Founder Must Understand Term Sheets

Pakistan’s startup ecosystem has transformed in the last five years. With over 80 active venture funds, angel networks in Islamabad, Lahore, and Karachi, and the arrival of Shark Tank Pakistan bringing mainstream attention to early-stage investing, more founders than ever are sitting across the table from investors. Yet, there is a knowledge gap that hurts founders disproportionately: legal and financial literacy around investment agreements.

Here is the uncomfortable reality: investors negotiate term sheets for a living. You, as a founder, might see one or two in your entire entrepreneurial journey before a liquidity event. That asymmetry means even fair-minded investors hold an advantage—not because they intend to exploit you, but because they understand the long-term implications of every clause. A term sheet Pakistan startup founders sign today can determine who controls the board three years from now, how much you personally earn in an exit, and whether you can raise your next round without the investor’s permission.

This is not fear-mongering. It is preparation. And preparation is what separates founders who build generational companies from those who lose control of their own vision.

🧠 Insider Insight from Shark Tank Pakistan: On the show, Sharks often make verbal offers that sound simple—”I will give you 1 crore for 20% equity.” But what the cameras do not always show is that the final term sheet includes protective provisions, board seat requirements, and sometimes royalty components that dramatically change the effective cost of that capital. A 20% equity offer is almost never just 20% equity.

What Exactly Is a Term Sheet? Breaking It Down

At its core, a term sheet is a blueprint. Think of it as the architectural drawing before the construction contract. It sets out the major commercial and governance terms that will later be fleshed out in the definitive agreements—the Share Subscription Agreement (SSA), Shareholders’ Agreement (SHA), and amended articles of association.

In Pakistan, a term sheet is presumptively non-binding under the Contract Act 1872, except for specific clauses that the parties explicitly agree shall be binding. Typically, three sections carry legal weight even before the final contracts are signed:

- Confidentiality: You cannot disclose the investor’s proposed terms to other potential investors or the public.

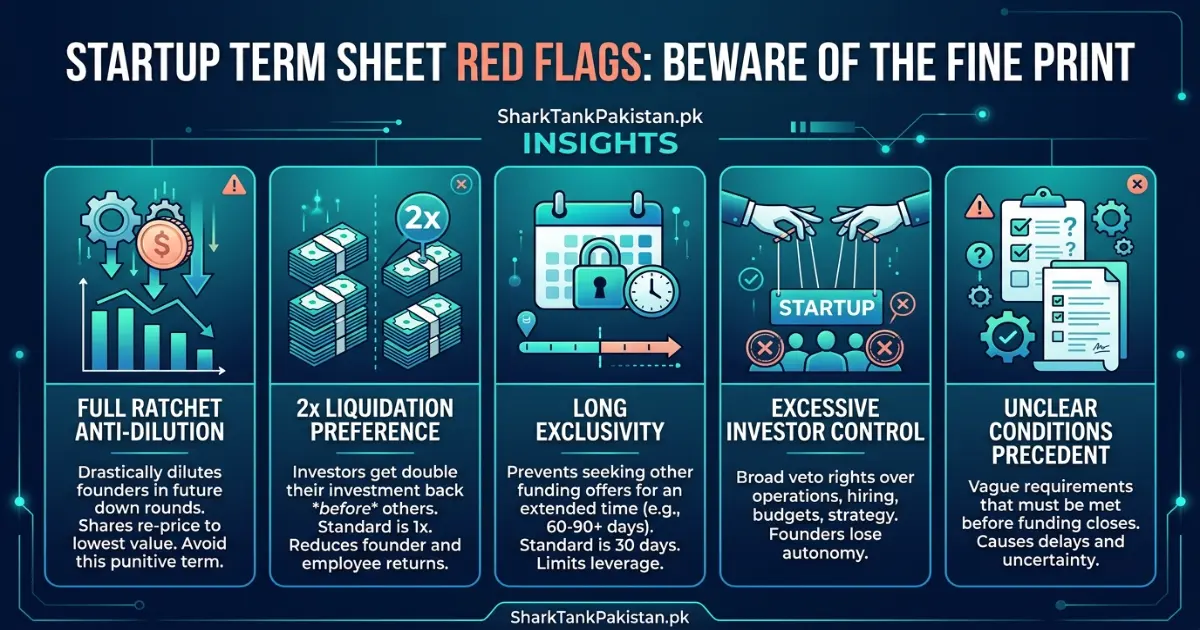

- Exclusivity (No-Shop): For a defined period—usually 30 to 60 days—you agree not to solicit or entertain offers from other investors.

- Expenses: Who pays for legal and due diligence costs if the deal falls through.

Everything else—valuation, equity percentage, board composition, liquidation preferences—is a statement of intent. Morally significant? Absolutely. Legally enforceable? Not until the definitive agreements are executed. This distinction is critical because Pakistani founders sometimes treat the term sheet as the final deal and stop negotiating too early. Do not make that mistake.

Key Components of a Term Sheet Every Founder Must Scrutinize

Not all clauses are created equal. Here are the sections that deserve your deepest attention—the ones that, if misunderstood, can haunt you for years.

1. Valuation and Investment Amount

This is what founders fixate on, and understandably so. The term sheet will state a pre-money valuation (what your company is worth before the investment) and the investment amount. Together, these determine the equity percentage the investor receives. For example, a PKR 5 crore investment on a PKR 20 crore pre-money valuation gives the investor 20% equity (5 / 25 post-money).

But here is what most Pakistani founders miss: the headline valuation can be misleading if the term sheet includes option pool top-ups that dilute founders before the investor’s shares are issued. Always ask: is the employee stock option pool included in the pre-money or created post-investment? In Shark Tank Pakistan, Sharks frequently ask founders to carve out additional equity for future hires—this effectively reduces the founder’s ownership more than the raw percentage suggests.

2. Liquidation Preference

This is arguably the most important economic term after valuation. Liquidation preference determines who gets paid first—and how much—in the event of a sale, merger, or winding up. A standard “1x non-participating” preference means the investor gets their money back before founders receive anything, and then converts to ordinary shares for the remaining distribution. A “2x participating” preference—rare but dangerous—means the investor gets double their investment back and then also shares in the remaining proceeds. For a Pakistani founder, agreeing to anything beyond 1x non-participating should require very strong justification and excellent legal advice.

3. Board Composition and Voting Rights

Control is not just about equity percentage. A term sheet often specifies how many board seats the investor receives, whether they have veto rights over major decisions (hiring a CEO, raising more capital, selling the company), and what constitutes a “reserved matter.” In Pakistan’s private limited company structure—governed by the Companies Act 2017—board composition directly affects who controls the strategic direction. A founder with 60% equity but only one board seat out of three can still lose operational control.

4. Anti-Dilution Protection

If your next funding round happens at a lower valuation (a “down round”), anti-dilution clauses protect the investor by adjusting their shareholding—usually by issuing them additional shares from the founders’ pool. There are two types: full ratchet (harsh—adjusts the price to the new lower price entirely) and weighted average (more balanced—adjusts based on the amount raised and the price difference). For Pakistani startups operating in volatile market conditions, weighted average is the founder-friendly standard. Full ratchet is a red flag unless the investor brings extraordinary strategic value.

5. Founder Vesting and Lock-In

Investors want to ensure founders stay committed. A typical term sheet includes a vesting schedule for founder shares—often four years with a one-year cliff—meaning if you leave before twelve months, you forfeit all unvested equity. This is standard and reasonable. What is less reasonable is an indefinite lock-in period that prevents founders from selling any shares even years after the investment. Negotiate a fair balance: investors deserve protection, but founders deserve eventual liquidity.

| Clause | Founder-Friendly | Investor-Friendly | Red Flag |

|---|---|---|---|

| Liquidation Preference | 1x non-participating | 1x participating (capped) | 2x+ participating (uncapped) |

| Anti-Dilution | Weighted average (broad-based) | Weighted average (narrow-based) | Full ratchet |

| Board Control | Founder majority + 1 investor seat | Equal split + independent director | Investor majority without performance triggers |

| Founder Vesting | 4-year, 1-year cliff, accelerated on exit | 4-year, 1-year cliff, no acceleration | Vesting resets on each funding round |

| Exclusivity Period | 30 days | 45–60 days | 90+ days with automatic renewal |

| Drag-Along Rights | Threshold: 70%+ shareholder approval | Threshold: 50%+ including investor consent | Investor can trigger unilaterally |

Term Sheet vs. Final Agreement vs. MOU: What Is the Difference?

Pakistani founders frequently confuse these three documents. Each serves a distinct purpose, and mixing them up can create serious legal exposure.

| Document | Binding? | Typical Length | Purpose |

|---|---|---|---|

| Term Sheet | Mostly non-binding (except confidentiality, exclusivity, expenses) | 2–6 pages | Summarize key commercial terms; align expectations before legal drafting |

| MOU (Memorandum of Understanding) | Can be binding or non-binding depending on wording | 3–10 pages | Broader statement of mutual intent; often used in strategic partnerships, not pure equity deals |

| Share Subscription Agreement (SSA) + Shareholders’ Agreement (SHA) | Fully binding and enforceable | 40–100+ pages combined | Definitive legal contracts governing the investment, rights, obligations, and exit mechanisms |

In the Pakistani context, MOUs are more common in family business transitions, joint ventures with Chinese or Gulf partners, and government-linked projects. For a pure equity fundraising round—whether from a VC, an angel network, or a Shark—the term sheet is the correct starting point, not an MOU.

How Shark Tank Pakistan Deals Translate into Real Term Sheets

If you have watched Shark Tank Pakistan, you have seen the dramatic moment: a Shark says, “I am offering you PKR 1.5 crore for 15% equity.” The founder hesitates. The music swells. They shake hands. But what happens after the cameras stop rolling?

The verbal offer on the show is essentially an oral term sheet. It captures the headline numbers—investment amount and equity percentage—but none of the protective provisions, governance terms, or conditions precedent that a written term sheet includes. Behind the scenes, the Shark’s legal team drafts a full term sheet that almost always includes:

- A due diligence condition (the deal is off if the founder’s revenue claims do not check out)

- Board observation or seat rights

- Information rights (monthly management accounts, annual audited financials)

- Restrictions on founder salary increases and related-party transactions

- Tag-along and drag-along provisions

This is not deception—it is standard practice. The lesson for Pakistani founders: never assume the on-air handshake is the final deal. It is the starting point of a negotiation that continues through the term sheet stage and into the definitive agreements. Several Shark Tank Pakistan contestants have publicly shared that their final signed deals differed materially from what was discussed on stage after due diligence revealed discrepancies or after legal negotiations refined the terms.

Common Mistakes Pakistani Founders Make When Reviewing Term Sheets

Over years of observing the Pakistani startup ecosystem, certain patterns emerge. Here are the mistakes that repeatedly cost founders money, control, or both.

Mistake 1: Focusing Only on Valuation

A high valuation feels like winning. But a PKR 30 crore valuation with aggressive liquidation preferences, full ratchet anti-dilution, and investor veto rights over future fundraising is far worse than a PKR 20 crore valuation with clean, founder-friendly terms. Valuation is vanity; terms are sanity. This is especially true in Pakistan, where follow-on funding rounds are harder to secure than in Silicon Valley or Bangalore—if you are locked into punitive terms from your seed round, Series A investors may demand those terms be restructured before they invest, and that restructuring almost always comes out of the founder’s equity.

Mistake 2: Not Hiring a Startup-Specialist Lawyer

Your family lawyer who handled your father’s property transfer is not the right person to review a venture capital term sheet. Pakistan now has several law firms and independent counsel with genuine startup investment experience—particularly in Karachi and Lahore. Their fees (typically PKR 150,000 to PKR 500,000 for a full term sheet review and negotiation) are a fraction of what a bad clause can cost you downstream. This is not an expense; it is insurance.

Mistake 3: Signing the Exclusivity Clause Without a Timeline

An open-ended or excessively long exclusivity period traps you. If the investor drags their feet on due diligence, you cannot talk to other potential investors. Always negotiate a firm end date—30 to 45 days is standard—and require an extension to be mutual and in writing. If the investor cannot complete due diligence in that window, you should be free to walk.

Mistake 4: Ignoring the “Conditions Precedent” Section

Term sheets often list conditions that must be satisfied before the investment closes—regulatory approvals, key customer contracts, hiring a CFO, or restructuring the corporate entity. If these conditions are unrealistic or entirely within the investor’s discretion, the deal can collapse without the investor ever breaching a binding obligation. Read this section line by line and push back on conditions you cannot control.

Mistake 5: Assuming Verbal Promises Are Enforceable

If a Shark or investor tells you, “Don’t worry about that clause—we would never actually enforce it,” and that assurance is not reflected in the written term sheet, it does not exist. Pakistani courts enforce written contracts, not dinner conversations. If an investor is genuinely flexible on a point, they will have no objection to writing that flexibility into the document.

Situation-Based Guidance: Your Stage Determines Your Priorities

Not all founders should negotiate the same way. Your bargaining power, risk tolerance, and strategic priorities shift dramatically based on where your startup stands.

If You Are Pre-Revenue (Idea Stage or MVP Only)

At this stage, investors are betting on you and your vision, not on traction. Expect tougher terms: higher equity asks, stricter vesting schedules, and possibly a board seat. Your negotiation leverage is limited, but you should still push for weighted average anti-dilution and a reasonable vesting schedule. The one thing you must protect is the ability to raise a follow-on round without the investor’s veto—because you will almost certainly need more capital before profitability. Accept that the valuation will be modest. Focus on keeping the governance terms clean.

If You Are Generating Revenue (PKR 1–10 Crore Annual Run Rate)

You now have genuine leverage. Revenue traction changes the conversation because it reduces the investor’s perceived risk. At this stage, negotiate hard on: (1) valuation—you have data to justify a higher multiple, (2) liquidation preference—1x non-participating should be your floor, and (3) board composition—you should retain majority control. Investors will still want protective provisions, but they should be tied to objective performance triggers, not arbitrary discretion.

If You Are a First-Time Founder

You are at the highest risk of being out-negotiated simply because you do not know what you do not know. Two specific actions: first, find a mentor who has raised institutional capital in Pakistan before—someone who can walk you through a redlined term sheet. Second, use the SharkTankPakistan.pk Valuation Calculator to benchmark your ask against industry norms before you even start conversations. Walking into a negotiation with data is the fastest way to close the experience gap.

If You Are a Serial Entrepreneur with a Previous Exit

Investors will treat you differently—and term sheets will reflect that. You can reasonably request: fewer board controls, lighter information rights (quarterly instead of monthly reporting), and accelerated vesting on a change of control. You have earned the right to demand founder-friendly terms. Use that leverage, but do not overplay it; Pakistan’s ecosystem is small, and reputations travel fast.

How to Use SharkTankPakistan.pk Tools to Strengthen Your Position

One of the most common reasons Pakistani founders accept unfavourable term sheets is that they lack independent data on what is “market standard.” They rely entirely on the investor’s framing. SharkTankPakistan.pk hosts several free tools designed to close this information gap.

Startup Valuation Calculator: Before you receive a term sheet—ideally before you even pitch—input your revenue, growth rate, industry, and asset base into the calculator. It provides a data-driven valuation range based on the methodologies most Pakistani investors use (revenue multiples for tech companies, asset-based approaches for traditional businesses, and DCF for cash-flow-positive operations). When an investor proposes a PKR 8 crore valuation and your calculator output suggests PKR 12–15 crore based on comparable transactions, you have a foundation for a respectful, evidence-based counteroffer.

Equity Dilution & Loan Calculator: Model out how the proposed equity split affects your ownership through one or two future funding rounds. Many founders look only at the immediate dilution (e.g., “I am giving up 20%”) without projecting what happens when the next investor takes another 15–20%. The calculator shows you the compounding effect so you can negotiate today with tomorrow in mind.

Term Sheet Clause Library (Coming Soon): Bookmark this resource. It will provide plain-English explanations of every clause commonly found in Pakistani term sheets, along with founder-friendly, neutral, and investor-friendly examples so you can see exactly where your offer falls on the spectrum.

FAQs: Term Sheets and Investment Agreements in Pakistan

Is a term sheet legally binding in Pakistan?

Mostly no. Under the Contract Act 1872, a term sheet is presumptively non-binding except for specific clauses the parties designate as binding—typically confidentiality, exclusivity (no-shop), and expense provisions. The commercial terms become binding only when the definitive agreements (SSA and SHA) are executed.

How much equity do Sharks typically take on Shark Tank Pakistan?

Based on aired deals, Shark Tank Pakistan investors typically seek between 10% and 35% equity, with 15–25% being the most common range. The percentage varies significantly based on the startup’s stage, revenue, and the perceived risk. Early-stage, pre-revenue companies face higher equity asks.

Do I need a lawyer to review a term sheet in Pakistan?

Yes—specifically a lawyer with startup investment experience, not a general practitioner. A competent review typically costs PKR 150,000–500,000, which is a fraction of what a single unfavourable clause can cost you in a future funding round or exit. This is non-negotiable protection.

What is the difference between a term sheet and a shareholders’ agreement?

A term sheet is a brief, mostly non-binding summary of key commercial terms. A shareholders’ agreement (SHA) is a comprehensive, fully binding legal contract that governs the relationship between shareholders, including voting rights, transfer restrictions, dispute resolution, and exit mechanisms. The SHA typically runs 40–80+ pages.

Can a term sheet offer from Shark Tank Pakistan fall through after the show?

Yes, and it happens regularly—not just in Pakistan but across all Shark Tank franchises. Deals can collapse during due diligence if the founder’s claims about revenue, IP ownership, or market traction cannot be verified. Roughly 30–40% of on-air deals do not close on the original terms or at all.

What is a liquidation preference in simple terms?

It determines who gets paid first when the company is sold or wound up. A “1x non-participating” preference means the investor recovers their investment amount first, and any remaining proceeds are distributed among all shareholders. This is the standard, founder-friendly baseline in Pakistan.

How long does it take to go from term sheet to money in the bank in Pakistan?

Typically 6 to 12 weeks, assuming no major issues arise during due diligence. The timeline includes legal drafting, negotiation of definitive agreements, completion of due diligence, satisfaction of conditions precedent, and regulatory filings with the SECP. Complex deals or those involving foreign investors may take longer.

What should I do if I receive multiple term sheets?

First, avoid signing any exclusivity clause until you have compared offers. Evaluate each term sheet holistically—not just valuation but also governance terms, investor reputation, and strategic value the investor brings. Use the competition to negotiate better terms, but do so transparently and respectfully.

A Real-World Scenario: What a Pakistani Term Sheet Looks Like in Practice

Let us walk through a realistic example. A Lahore-based B2B SaaS startup with PKR 3.5 crore in annual recurring revenue receives a term sheet from a Karachi-based venture fund. The key terms:

- Investment: PKR 5 crore

- Pre-money valuation: PKR 20 crore (roughly 5.7x ARR—reasonable for a growing SaaS company in Pakistan)

- Equity: 20% (5 / 25 post-money)

- Liquidation preference: 1x non-participating

- Board: 3 seats—2 founders, 1 investor

- Anti-dilution: Weighted average (broad-based)

- Founder vesting: 4 years, 1-year cliff, with acceleration on change of control

- Exclusivity: 45 days

This is a clean, market-standard term sheet. The founders should feel comfortable proceeding—but they should still have it reviewed by counsel and should negotiate one addition: a clause specifying that the investor’s veto rights over future fundraising do not apply to rounds raised at or above the current valuation. This protects their ability to bring in strategic capital without obstruction.

Now contrast this with a problematic version of the same offer: same valuation, but with 2x participating liquidation preference, full ratchet anti-dilution, and a clause giving the investor the right to block any future fundraising at their sole discretion. The headline numbers look identical, but the downstream consequences are worlds apart. The founders would be significantly better off taking a lower valuation with cleaner terms.

Put This into Practice: Your Term Sheet Action Plan

Reading about term sheets is step one. Here is what to actually do:

Step 1: Open the SharkTankPakistan.pk Valuation Calculator and run your numbers. Know your realistic valuation range before any investor proposes one.

Step 2: Build a one-page “term sheet cheat sheet” for yourself listing your red lines—the terms you will not accept under any circumstances. For most Pakistani founders, those should include: full ratchet anti-dilution, uncapped participating liquidation preferences above 1x, and investor control over founder salary without performance linkage.

Step 3: Identify and brief a startup-specialist lawyer before you receive a term sheet. The worst time to search for counsel is when a 30-day exclusivity clock is already ticking.

Step 4: When the term sheet arrives, read it yourself first. Highlight every clause you do not fully understand. Then send it to your lawyer with your notes. Do not outsource your comprehension—stay engaged.

Step 5: Negotiate collaboratively, not adversarially. The investor is about to become your business partner. Frame your counterproposals around fairness and long-term alignment, not short-term wins.

⚡ Your Fast-Track Cheat Sheet: Top 3 Takeaways

- Terms matter more than valuation. A clean term sheet with a modest valuation will serve you far better than a headline-grabbing number loaded with punitive clauses. Always model the downstream impact of liquidation preferences, anti-dilution, and board controls before you celebrate the valuation.

- Never sign a term sheet without a startup-specialist lawyer. The PKR 150,000–500,000 you spend on legal review is the cheapest insurance you will ever buy. One bad clause—full ratchet anti-dilution, uncapped participating preference, or an open-ended exclusivity period—can cost you your company.

- A term sheet is the beginning, not the end. Whether on Shark Tank Pakistan or in a venture fund boardroom, the offer is a starting point for negotiation. Use the calculators on SharkTankPakistan.pk to arm yourself with data, protect your red lines, and treat the negotiation as the foundation of a relationship that may define the next decade of your entrepreneurial journey.