DCF Valuation Pakistan: How to Estimate Your Startup’s Worth With Confidence

Quick Answer: The DCF method values your startup by forecasting future free cash flows and discounting them back to today’s rupees, using a rate that reflects the risk of doing business in Pakistan. For Shark Tank Pakistan, a conservative DCF—paired with realistic growth assumptions—tells a much stronger story than an inflated revenue multiple.

Most Pakistani founders I meet are obsessed with revenue multiples. Someone tells them “tech startups in the US are valued at 10x revenue,” and they immediately apply that to their Lahore-based SaaS with PKR 15 million in bookings. That approach crumbles in front of the Sharks. If you want to walk into a pitch with a defensible number, you need to understand DCF valuation Pakistan — not as a theoretical exercise, but as a practical tool for putting a price tag on your future.

I’ve coached dozens of founders preparing for Shark Tank Pakistan and local angel rounds. The ones who get a deal almost always show they understand the nuts and bolts of cash flow, not just a hockey-stick graph. This guide is built specifically for the Pakistani ecosystem: currency volatility, inflation, high cost of capital, and all. You’ll learn how to calculate your startup’s worth using DCF, avoid the mistakes that kill valuations, and use the SharkTankPakistan.pk DCF calculator to generate a number that holds up under interrogation.

Why DCF Matters Right Now for Pakistani Entrepreneurs

Pakistan’s startup funding landscape has shifted. The days of easy valuation markups on hype are fading. Both local VCs and the Sharks on Shark Tank Pakistan are scrutinizing unit economics and real cash generation. DCF forces you to answer the question every investor asks eventually: “When will this business actually produce free cash, and how much risk do I take by waiting?”

In a market where the discount rate is heavily influenced by the State Bank’s policy rate (currently high), inflation, and country risk premiums, a DCF tailored to Pakistan gives a much more honest picture than a simplified multiple. That honesty is what sets apart a credible founder from someone who just Googled “startup valuation formula.”

The DCF Valuation Method: A Step-by-Step Breakdown for Pakistani Founders

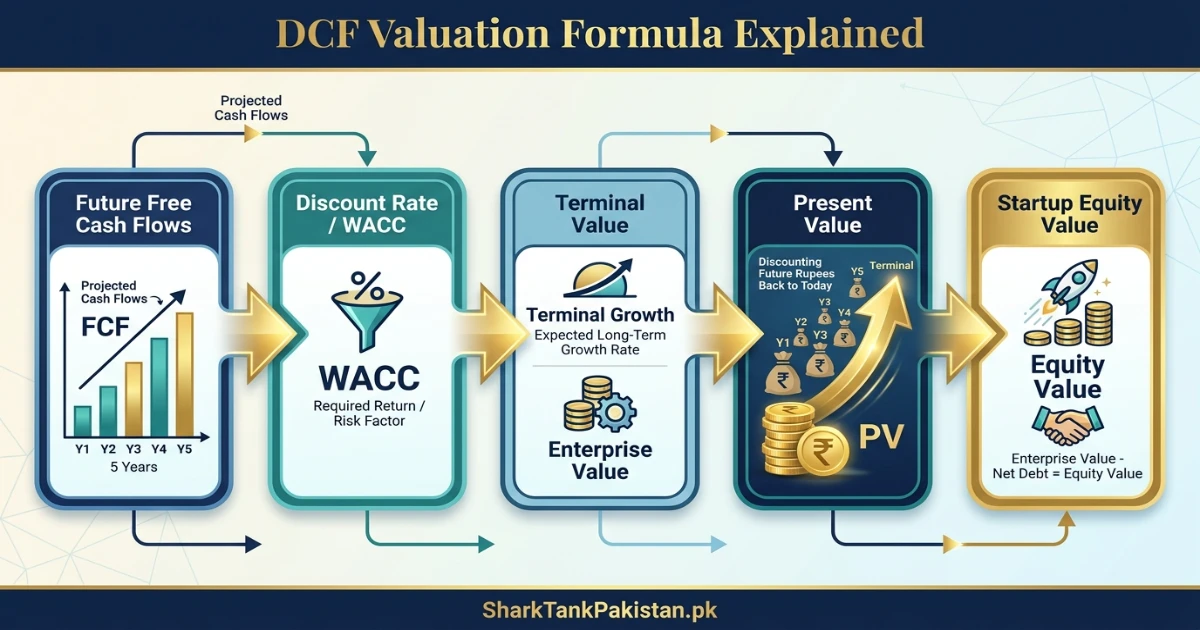

At its core, DCF (Discounted Cash Flow) works on the principle that a rupee tomorrow is worth less than a rupee today. To value your startup, you project its free cash flows for the next 5 to 7 years, calculate a “terminal value” beyond that, and discount everything back to present value using a rate that reflects risk. Let’s walk through it with the local context baked in.

Step 1: Forecast Free Cash Flows (FCF) — Not Revenue

Free cash flow is the cash your business generates after covering operating expenses and capital expenditures. For a Pakistani startup, this means you need to model:

- Revenue growth year by year (be realistic — inflation alone can bloat top-line numbers).

- Operating costs, including fuel/energy expenses that fluctuate wildly in Pakistan.

- Working capital changes (inventory buildup, receivables delays common in local B2B).

- Capital expenditures for equipment, tech infrastructure, or expansion into cities like Karachi, Lahore, Islamabad.

If you’re pre-revenue, base forecasts on a granular bottom-up analysis: number of customers, average order value, conversion rates. Avoid the temptation to claim 200% year-on-year growth indefinitely — the Sharks will tear that apart.

Step 2: Determine a Realistic Discount Rate (WACC) for Pakistan

The discount rate is where many Pakistani founders stumble. In international textbooks, you’ll see WACC (Weighted Average Cost of Capital) around 8–12%. In Pakistan, a reasonable discount rate for a startup often sits between 18% and 28%, depending on the industry and stage. Why? Because:

- The risk-free rate (based on Pakistan Investment Bonds) is already high.

- Equity risk premium must account for currency depreciation, political instability, and governance concerns.

- Startups carry additional operational risk — unproven business models, thin management depth.

Using a 10% discount rate for a Pakistani e-commerce startup would grossly overvalue it. A Shark would immediately ask, “What’s your cost of equity? Have you factored in country risk?” A good starting point: take the 10-year PIB yield, add a 6–8% equity risk premium, and layer on a startup-specific risk adjustment of 4–8%.

Step 3: Calculate the Terminal Value — The Pakistani Reality Check

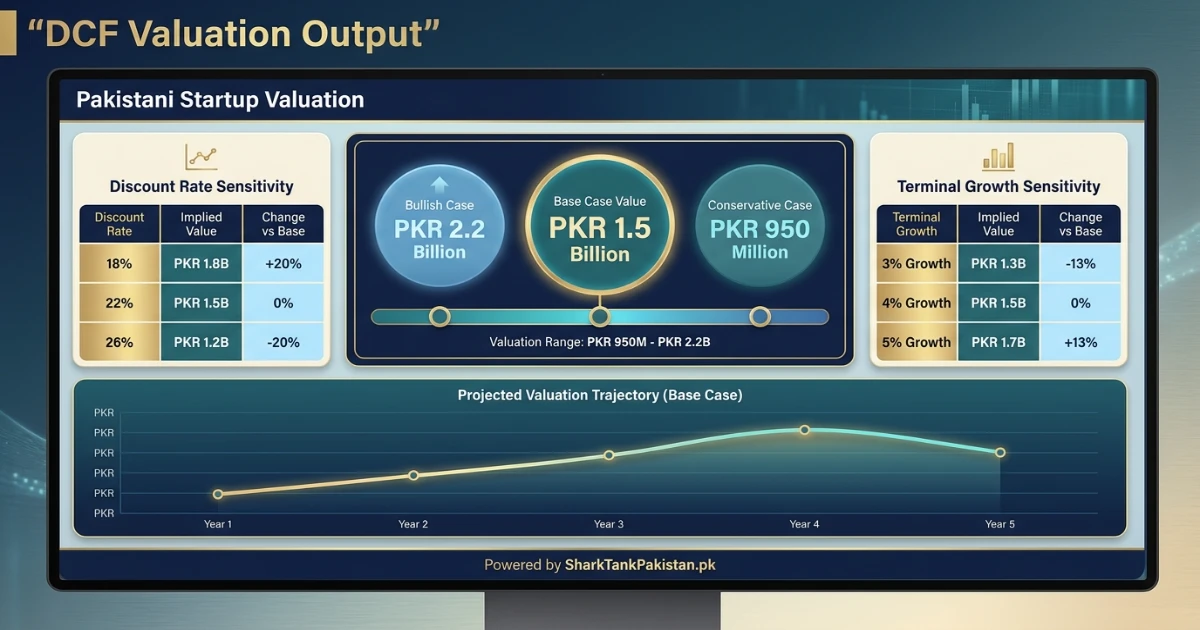

After your explicit forecast period (say 5 years), you need to estimate the value of all cash flows beyond that. Two common methods: perpetuity growth model (Gordon Growth) and exit multiple. In Pakistan, the perpetuity growth rate should rarely exceed 4-5%, roughly mirroring long-term nominal GDP growth plus inflation. An exit multiple (e.g., 8x EBITDA) might be more intuitive, but needs sector justification. The terminal value often accounts for 60–80% of the total DCF valuation, so a small change in assumptions can swing your number wildly. That’s why transparency matters more than precision.

Step 4: Discount and Sum — The Enlightening Final Number

Discount each year’s projected FCF and the terminal value back to today using your chosen discount rate. The sum is your enterprise value. Subtract net debt (or add cash) to get equity value — the worth of your startup’s shares. If your forecast is solid and your discount rate honest, the resulting number often feels lower than what you expected. That discomfort is healthy — it forces you to stress-test your business model before the Sharks do it for you.

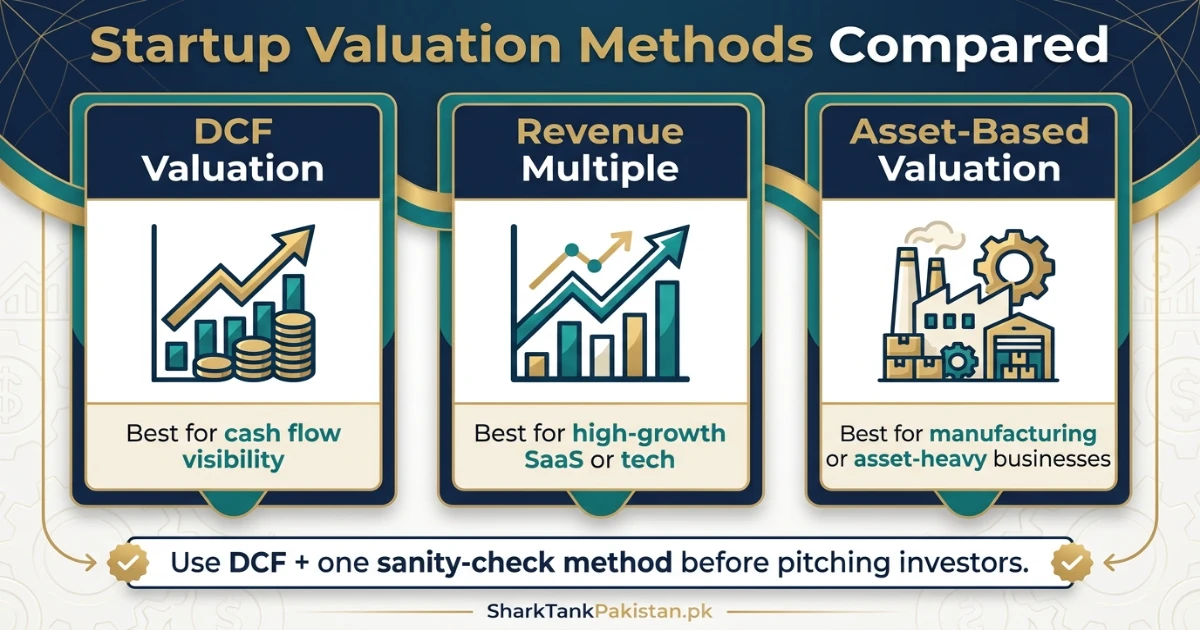

DCF vs. Other Valuation Methods — Which One Should You Present in the Tank?

You might wonder why bother with DCF when a simple revenue multiple seems quicker. Here’s a comparison tailored to the Pakistani startup scene.

| Method | How It Works | Best For | Weakness in Pakistan |

|---|---|---|---|

| DCF (Discounted Cash Flow) | Projects future cash flows, discounts to present | Startups with some operating history, clear unit economics, long-term view | Highly sensitive to discount rate and terminal growth assumptions; can undervalue asset-light tech if discount rate is too high |

| Revenue Multiple | Applies a multiple (e.g., 3x–8x) to current or next-year revenue | High-growth tech, SaaS with recurring revenue | Ignores cash flow and profitability; overvalues startups that burn cash with no path to profit; doesn’t adjust for local macro risk |

| Asset-Based Valuation | Sums up net asset value (tangible assets minus liabilities) | Manufacturing, real estate, brick-and-mortar retail | Completely misses intangible value (brand, tech, user base); rarely reflects true worth of a digital startup |

In Shark Tank Pakistan, a sophisticated answer combines DCF with a sanity-check multiple. You might say, “Our DCF valuation comes to PKR 85 million, and that aligns with a 4.5x revenue multiple given our growth trajectory — but we’re open to discussing the assumptions.” That shows depth.

The Sharks rarely accept DCF at face value. They immediately reverse-engineer your discount rate and terminal growth. One founder from Season 1 (a Karachi-based logistics startup) used a 15% discount rate and got grilled on why he thought his business was less risky than a government bond. Prepare a sensitivity table showing value under different discount rates — that kind of preparation screams maturity.

Situation-Based Adjustments: DCF for Different Startup Profiles

How you apply DCF changes dramatically based on where you stand. Let’s tailor the approach for two common reader profiles.

If You’re Pre-Revenue or Idea-Stage

Traditional DCF is extremely speculative without revenue. Instead, lean on a bottom-up total addressable market (TAM) approach baked into your cash flow forecast. Factor in conversion rates from a pilot, waitlist signups, or analogous benchmarks. Use a higher discount rate (24–30%) to reflect execution risk. The Sharks will want to see a clear, defensible path to first revenue, not just a discounted fantasy. In this case, the DCF exercise is more about demonstrating logical thinking than producing a precise number.

If You’re Generating Steady Cash Flows (Traditional Business or SME)

DCF truly shines here. A Pakistani textile exporter, a food processing unit, or a regional retail chain with audited financials can produce credible forecasts. Use historical growth rates, moderate terminal growth, and a discount rate informed by actual borrowing costs. The valuation will feel grounded. When you present this to a Shark, you can clearly separate the “asset play” from the growth story.

When You’re Pitching on Shark Tank Pakistan vs. a Private Angel Investor

On the show, you have minutes. You can’t walk through a full DCF spreadsheet. But having the DCF-derived number — and being able to explain the two key levers (discount rate and terminal growth) — gives you instant credibility. With an angel or VC in a longer meeting, you’ll have time to present the detailed model. Always bring a printed one-pager with your assumptions.

Common Mistakes Pakistanis Make with DCF (and How to Fix Them)

I’ve reviewed dozens of DCF models from Pakistani founders. The same errors show up again and again. Here are the five deadliest, contextualized for our market.

- 1. Using an unrealistically low discount rate. Just because a US textbook says 10% doesn’t mean it applies in Karachi. If your discount rate is below 16%, you’re essentially claiming your startup is less risky than a blue-chip Pakistani corporate. Fix it by anchoring to the KIBOR or PIB yield and adding country + startup risk.

- 2. Forecasting in USD while incurring costs in PKR (or vice versa). Currency mismatch distorts margins. If your revenue is in dollars but local costs are in rupees, model the inflation and devaluation explicitly. A static exchange rate assumption is a red flag.

- 3. Ignoring working capital drains. Pakistani businesses often suffer from delayed payments (especially B2B and government contracts). Your DCF must account for the cash trapped in receivables. Build in realistic debtor days.

- 4. Overestimating terminal growth. Using a 6% or 7% perpetual growth rate in a country where long-term GDP growth hovers near 3-4% (adjusted for population) is wishful thinking. Cap it at 4-5% max.

- 5. Treating DCF as the final answer. DCF is a conversation starter, not a decree. Don’t cling to your number rigidly. Show the range, acknowledge the sensitivity, and be open to negotiation.

When NOT to Rely on DCF

DCF can mislead if your business has no clear path to positive free cash flow in the forecast horizon. For a deep-tech startup burning cash for R&D with uncertain monetization, a venture capital method (estimating exit value and working backwards) might fit better. Also, if your startup is asset-heavy and has significant liquidation value, an asset-based approach combined with DCF provides a safety floor. Always cross-check with at least one other method.

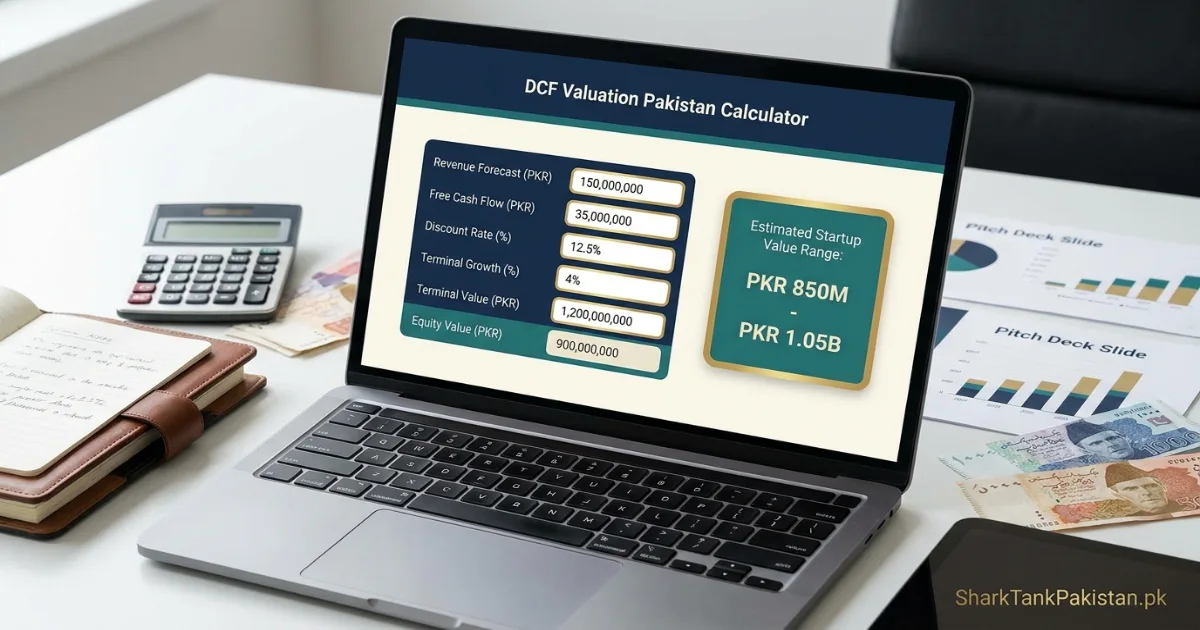

How to Use the SharkTankPakistan.pk DCF Valuation Calculator

We built a dedicated DCF calculator specifically for the Pakistani entrepreneur. Head over to the DCF Valuation Calculator and you’ll find fields tailored to our context: you can input revenue projections in PKR, set a discount rate range, select terminal growth assumptions, and even adjust for inflation. The tool instantly gives you a valuation range, which you can then stress-test by tweaking variables. It’s the fastest way to turn this article into a usable number for your pitch deck.

Try this: input your cautious base case, then a bullish case with 20% lower discount rate, and see the swing. That spread is what you’ll need to defend. Print the output and keep it in your data room.

Real-World Example: Pakistani E-Commerce Startup “KaryanaDirect”

Let’s ground this with a hypothetical but realistic case. KaryanaDirect is an online grocery delivery platform operating in Lahore and planning expansion to Islamabad and Faisalabad. In 2026, they generated PKR 45 million in revenue with a net loss, but unit economics are improving. They project the following free cash flows (in PKR millions) over the next 5 years: Year 1: -8, Year 2: 2, Year 3: 9, Year 4: 18, Year 5: 28. They assume a terminal growth rate of 4%. Using a discount rate of 22% (reflecting e-commerce execution risk and Pakistan macro), the DCF spits out an enterprise value of approximately PKR 152 million. After adjusting for a small debt, equity value comes to PKR 148 million.

When they walk into the Tank asking for PKR 15 million for 10% equity, that implies a post-money valuation of PKR 150 million — right in line with their DCF. The Sharks can then debate assumptions, but the starting point is rational and well-supported.

FAQs About DCF Valuation in Pakistan

- 1. What discount rate should I use for a Pakistani startup?

- Most Pakistani startups should use a discount rate between 18% and 28%, depending on industry risk, stage, and macroeconomic factors. Anchor to the risk-free rate (PIB yield around 12-13%) and add equity risk and startup-specific premiums.

- 2. Can I use DCF if my startup is not yet profitable?

- Yes, but with caution. You’ll need a credible path to profitability within your forecast horizon. Use bottom-up assumptions and clearly show when free cash flow turns positive. The Sharks will scrutinize this inflection point heavily.

- 3. How do Shark Tank Pakistan investors usually value startups?

- Sharks often blend methods—revenue multiples for high-growth tech, DCF for businesses with cash flow visibility, and sometimes asset-based for traditional firms. They heavily discount projections if the team lacks execution proof. Expect them to offer a lower valuation than your DCF suggests.

- 4. Is DCF the best valuation method for a Pakistani e-commerce startup?

- DCF works well if the e-commerce startup has unit economics that show improving margins. However, combine it with a revenue multiple check because e-commerce valuations are often market-comparison driven. Use DCF to sanity-check the multiple.

- 5. How do I factor inflation and currency risk into my DCF?

- Incorporate inflation by escalating costs and revenues realistically, but more importantly, adjust your discount rate upward to reflect purchasing power risk. If cash flows are in PKR, the discount rate already absorbs some devaluation risk. Explicitly note your assumptions.

- 6. What free tools can I use for DCF valuation in Pakistan?

- The SharkTankPakistan.pk DCF Valuation Calculator is designed specifically for local founders. It includes preset country risk parameters and guides you through each step. You can also build a basic model in Excel, but our tool saves hours.

- 7. Do Sharks on Shark Tank Pakistan understand DCF?

- Absolutely. The Sharks are experienced investors who can dissect a DCF in seconds. They care about the logic behind your numbers, not just the final value. Be prepared to defend every input.

- 8. Should I present the DCF valuation or just the final number in my pitch?

- Present the final valuation clearly, but have the DCF summary ready. Verbalize the key assumptions: “We used a 24% discount rate and 4% terminal growth, leading to an equity value of PKR 85 million.” This signals depth without overwhelming.

Your Fast-Track Cheat Sheet: Top 3 Actions to Take

- Build a conservative DCF model today. Pull your last two years’ financials (or bottom-up projections), set a realistic discount rate (18–28%), and calculate your startup’s value range. Share it with a mentor for a gut check.

- Create a sensitivity table. Vary the discount rate by ±3% and terminal growth by ±1%. Note how valuation swings. This one document will separate you from 90% of pitchers.

- Test-drive the SharkTankPakistan.pk DCF Calculator. Input your numbers, get the range, and practice explaining the output in under 60 seconds. That’s your pitch-ready soundbite.