Gold Box Pakistan Shark Tank: The Interest-Based E-Commerce Pitch Explained in Full

Quick Answer: Gold Box Pakistan walked into the Shark Tank Pakistan tank with an e-commerce platform that lets customers buy products by paying in installments — but with a built-in interest component that makes each installment total higher than the upfront price. The pitch sparked heated debate among the sharks about whether this model qualifies as ethical, Shariah-compliant, or simply a rebranded version of conventional buy-now-pay-later debt. Here’s exactly how the pitch unfolded, what the numbers revealed, and what every Pakistani founder must understand before building an interest-laced consumer model.

If you’ve ever scrolled through a Pakistani e-commerce store and seen a “3 easy installments” tag, you’ve brushed up against the very business model that Gold Box Pakistan brought to the Shark Tank Pakistan stage. And if you’re an entrepreneur considering anything that involves deferred payments, markup, or “convenience fees,” this pitch is your case study — because it lays bare every tension point between consumer accessibility, investor appetite, and the elephant in the room for Pakistani businesses: Is charging interest on installment plans just smart fintech, or is it a reputational time bomb?

Gold Box Pakistan’s pitch didn’t just test the sharks’ wallets. It tested their principles. Some saw a scalable revenue engine. Others saw a model that might struggle to scale in a market where “interest” — however you dress it up — remains a deeply loaded word. In this article, we unpack the full pitch, the business mechanics, the sharks’ counterarguments, and the brutally practical lessons for anyone building a consumer finance-adjacent startup in Pakistan.

What Exactly Is Gold Box Pakistan? The Business Model Stripped Down

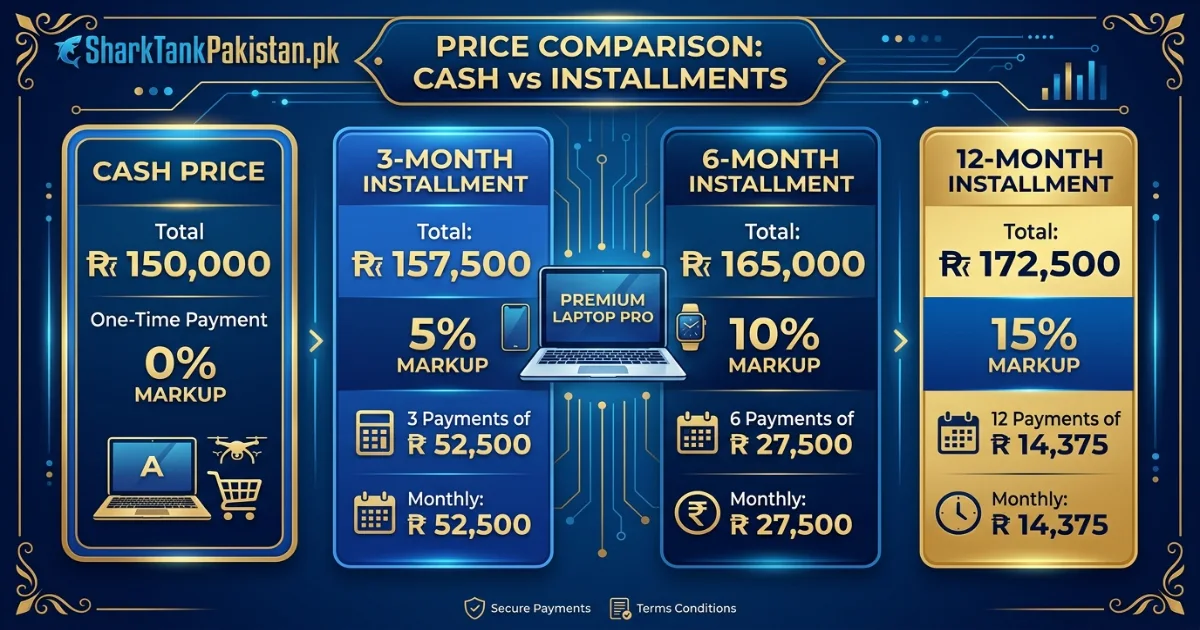

At its core, Gold Box Pakistan is an e-commerce platform that sells consumer goods — electronics, home appliances, lifestyle products — with a twist: customers don’t pay the full price upfront. Instead, they pay in monthly installments over 3, 6, or 12 months. But here’s the catch that became the focal point of the Gold Box Pakistan Shark Tank pitch: those installment payments include a markup — a percentage added on top of the base price — which the company frames as a “service fee” or “convenience charge,” but which the sharks immediately identified as functionally equivalent to interest.

The pitch revealed that Gold Box’s average markup ranged between 15% and 28% over the installment period, depending on the product category and repayment duration. On a Rs. 100,000 laptop, a customer opting for a 6-month plan might end up paying Rs. 118,000 to Rs. 128,000. That’s a tidy margin for the platform — and a significant extra cost for the customer. The founders argued this was simply the cost of convenience and credit access in a market where most consumers don’t have credit cards. The sharks weren’t all convinced.

How the Installment Math Actually Works

Let’s break down a real example from the pitch. Gold Box listed a smartphone with a cash price of Rs. 60,000. On a 3-month installment plan, the total repayment came to Rs. 68,400 — three payments of Rs. 22,800 each. That’s a 14% effective markup over 90 days. Annualized, that figure climbs well above 50%. The founders acknowledged the annualized rate but emphasized that their target customer — a salaried individual without access to bank credit — wasn’t thinking in APR terms. They were thinking about monthly affordability.

This is where the pitch got interesting. The sharks who pushed back weren’t questioning the math. They were questioning the optics. One shark asked point-blank: “If a bank offered this, you’d call it interest. Why should your customer call it anything else?”

Inside the Tank: How the Gold Box Pakistan Shark Tank Pitch Played Out

The Gold Box Pakistan founders entered the tank with confidence, asking for a substantial investment in exchange for a minority equity stake. They came armed with traction numbers — monthly active users, gross merchandise value, repeat purchase rates — and a narrative about democratizing access to quality products for Pakistan’s underbanked population. The initial reaction was positive. The sharks liked the user numbers and the clear product-market fit in a country where credit card penetration hovers around 2%.

Then the questions turned to the markup structure — and the room shifted. One shark, known for their directness on financial ethics, pressed the founders to explain how their model differed from a loan shark’s operation, apart from the branding. Another shark, more commercially focused, asked about default rates and collections infrastructure. The founders had answers — they maintained a default rate under 6% and used a combination of in-house collections and third-party recovery agents — but the ethical framing question lingered throughout the session.

The Deal — or Lack Thereof

After a tense back-and-forth, the outcome divided the panel. One shark made an offer contingent on restructuring the markup language and rebranding the fee structure to align more closely with Shariah-compliant murabaha principles. Another shark offered a lower valuation but with a strategic partnership that included access to a retail distribution network. A third shark opted out entirely, stating that while the business could make money, the model didn’t align with their personal investment thesis. The final outcome — whether a deal closed and at what terms — became one of the most discussed moments of the episode.

Interest-Based Installments vs Conventional E-Commerce: The Model Comparison

To understand what makes the Gold Box Pakistan pitch so instructive, you need to see how the model stacks up against standard e-commerce and other financing alternatives available to Pakistani consumers.

| Dimension | Gold Box Pakistan Model | Standard E-Commerce (Cash) | Bank Credit Card EMI | Shariah-Compliant Murabaha |

|---|---|---|---|---|

| Upfront Cost to Customer | Zero — pay over time with markup | 100% upfront | Zero — pay over time with interest | Zero — cost-plus deferred payment |

| Effective Annual Markup | 40%–70%+ annualized | 0% | 24%–42% typical in Pakistan | Varies; transparent profit margin |

| Customer Eligibility | Minimal checks; broad access | Anyone with cash | Credit score, income proof required | Varies by provider |

| Default Risk | Medium–high; in-house collections | None | Medium; bank collections infrastructure | Low–medium |

| Shariah Perception | Controversial; functionally interest | Neutral | Generally seen as interest (riba) | Structured as trade, not lending |

| Scalability in Pakistan | High if reputational risk managed | Limited by cash-on-delivery reliance | Capped by low credit card penetration | Growing but trust-dependent |

If You’re Building Something Similar: How the Advice Changes Based on Your Stage

Not every entrepreneur wrestling with the Gold Box Pakistan model is in the same position. Here’s how the strategic calculus shifts depending on where you stand.

If You’re Pre-Launch or Ideation Stage

You have the luxury of designing your fee structure from scratch. This is your window to build something that doesn’t just work financially but also passes the “explain it to your grandmother” test in a Pakistani cultural context. Consider structuring your markup as a transparent, fixed profit margin disclosed upfront — closer to a murabaha model — rather than a percentage that scales with time. The optics matter enormously at this stage because you haven’t yet built a brand that can absorb reputational hits. Early decisions about how you describe your fees will follow you into every investor meeting and customer review thread.

If You’re Already Generating Revenue With a Markup Model

You’re in Gold Box’s shoes. You have traction, but you also have a model that savvy customers and investors will scrutinize. Your priority should be compliance readiness and messaging refinement. Consult with a Shariah advisor — not necessarily to become fully Shariah-compliant overnight, but to understand where your model sits on the spectrum and what adjustments would be required to move toward a more widely accepted structure. Document everything. If a shark asks about your markup, you want a one-slide answer that shows you’ve thought about this, not a defensive scramble.

If You’re Pitching to Investors (Especially on Shark Tank Pakistan)

Anticipate the interest question. It will come. Prepare a response that doesn’t dodge the word but addresses it head-on with transparency and a clear differentiation strategy. The sharks who backed interest-adjacent models on international Shark Tanks did so because the founders could articulate exactly why their model was fair, sustainable, and ethically defensible. If you can’t do that in under 60 seconds, the conversation will spiral. Practice answering: “How is this different from a loan with interest?” until your answer is crisp, honest, and compelling.

Common Pitfalls & When to Ignore This Advice Entirely

Not every lesson from the Gold Box Pakistan Shark Tank pitch applies universally. Here’s where founders get tripped up — and when the standard advice might actually steer you wrong.

- Pitfall 1: Hiding the markup in vague language. Terms like “processing fee,” “platform charge,” and “service cost” may feel safer than “interest,” but they erode trust the moment a customer does the math. If your total repayment is 25% above the cash price, own it. Transparency is cheaper than reputation repair.

- Pitfall 2: Ignoring the Shariah conversation entirely. Even if your target market isn’t exclusively Muslim (though in Pakistan, it overwhelmingly is), the broader cultural norm treats interest as ethically suspect. Pretending this reality doesn’t exist is a strategic blind spot, not a clever positioning move.

- Pitfall 3: Assuming high default rates are sustainable. A 6% default rate sounds manageable in a pitch deck. In reality, in Pakistan’s consumer market — where collection infrastructure is thin and legal recourse is slow — defaults can spike unexpectedly during economic downturns. Build a buffer. Double it.

- Pitfall 4: Copying international BNPL models without localization. Klarna and Afterpay work in markets with robust credit bureaus and regulatory clarity. Pakistan’s ecosystem is different. What flies in Sweden or the US won’t necessarily translate to Karachi or Lahore without significant adaptation.

The Regulatory Reality: Where Pakistani Law Stands on Interest-Based E-Commerce

One question the sharks raised — and that any founder in this space must investigate — is where the regulatory line sits. Pakistan’s legal framework, shaped by both conventional banking laws and the Federal Shariat Court’s rulings on riba, creates a complex landscape for businesses that charge time-based markups to consumers. As of now, there is no specific e-commerce installment regulation that explicitly prohibits or permits the Gold Box Pakistan model. But that absence of clarity is itself a risk. Regulatory bodies, including the Securities and Exchange Commission of Pakistan and the State Bank, have shown increasing interest in fintech and consumer lending models. A regulatory shift — or a high-profile consumer protection case — could change the ground rules overnight.

Smart founders in this space treat regulatory ambiguity not as a green light but as a yellow one. They proactively engage legal counsel, document their fee structures meticulously, and build flexibility into their models so they can pivot if the regulatory winds shift. The sharks who showed interest in Gold Box Pakistan almost certainly factored this uncertainty into their valuation offers.

Put This Into Practice: Model Your Own Unit Economics

If the Gold Box Pakistan pitch has you rethinking your own e-commerce pricing structure — or planning a pitch of your own — the best thing you can do right now is run the numbers. Open a spreadsheet, or better yet, use the calculators we’ve built specifically for Pakistani founders navigating these exact decisions. Plug in your product cost, your desired markup, your installment periods, and your estimated default rate. See what your effective annualized return looks like. Then ask yourself honestly: if a shark put that number on screen in front of a national audience, would you be comfortable defending it?

Try the SharkTankPakistan.pk Equity & Loan Calculator to model different funding scenarios, or use our Startup Valuation Calculator to see how a markup-heavy revenue model might affect your company’s valuation in the eyes of investors. Numbers don’t lie — and in the tank, they’re all that stands between you and a deal.

Real-World Echoes: Other Pakistani Startups Navigating the Interest Question

Gold Box Pakistan isn’t alone in this gray zone. Several Pakistani startups operating in the buy-now-pay-later and installment-commerce space have faced similar scrutiny — from investors, customers, and social media. Some have successfully repositioned by obtaining Shariah advisory board certifications and restructuring their contracts as cost-plus-financing agreements. Others have quietly rebranded their fees while keeping the underlying math identical — a short-term fix that savvy consumers eventually notice. The ones that thrive long-term tend to be those that treat the ethical dimension not as a PR problem to be managed but as a product design constraint to be respected. That distinction — between managing perception and building integrity — is what separates a pitch that wins sharks from one that divides them.

Frequently Asked Questions About Gold Box Pakistan and Interest-Based E-Commerce

What is Gold Box Pakistan’s business model?

Gold Box Pakistan sells consumer products through installment plans that include a markup — typically 15% to 28% over the base price — structured as a convenience fee rather than explicitly labeled interest. Customers pay over 3, 6, or 12 months, making products accessible to those without credit cards, but at a significantly higher total cost than the upfront cash price.

Did Gold Box Pakistan get a deal on Shark Tank Pakistan?

The pitch resulted in mixed responses from the sharks. At least one shark made a contingent offer requiring restructuring of the fee model toward a more Shariah-aligned framework, while another shark declined citing reputational concerns around the interest-like markup structure. The final outcome became one of the season’s most debated investment decisions.

Is Gold Box Pakistan’s model Shariah-compliant?

This was the central tension of the pitch. In its original form, the model’s time-based markup is functionally similar to interest (riba), which makes Shariah compliance questionable. The sharks who engaged seriously with the pitch discussed restructuring toward a murabaha-style cost-plus model, which would involve a fixed, upfront profit disclosure rather than a time-scaled percentage.

How does Gold Box Pakistan compare to international BNPL services like Klarna?

While the surface model looks similar — pay over time — Gold Box Pakistan operates in a market with vastly different regulatory oversight, consumer credit infrastructure, and cultural attitudes toward interest. International BNPL companies often rely on merchant fees rather than consumer markups, whereas Gold Box’s model places the cost directly on the consumer through elevated installment totals.

What default rate did Gold Box Pakistan report on Shark Tank?

The founders reported a default rate below 6% during their pitch, supported by in-house collections processes and third-party recovery agents. However, default risk in Pakistan’s consumer market can be volatile, especially during economic downturns when collection infrastructure faces stress.

Can an interest-based e-commerce model succeed long-term in Pakistan?

Yes, commercially — but with significant caveats. The consumer demand for installment-based purchasing is enormous given Pakistan’s low credit card penetration. However, long-term success depends on navigating Shariah perception, potential regulatory changes, and brand trust. Models that transparently disclose costs and move toward structured trade-based financing are better positioned for sustainable growth.

What should I know before pitching an installment-commerce startup to Pakistani investors?

Be prepared to answer the “Is this interest?” question directly, with a clear, concise, and defensible explanation. Have your unit economics fully modeled, including annualized effective rates. Consider consulting a Shariah advisor before your pitch. Investors in Pakistan increasingly weigh ethical optics alongside financial returns, especially for consumer-facing models.

Where can I learn more about Shark Tank Pakistan pitches and investment strategies?

SharkTankPakistan.pk publishes in-depth pitch breakdowns, valuation calculator guides, and episode recaps covering every Shark Tank Pakistan deal, contestant strategy, and investor insight. Visit our Best Pitches section for detailed analyses and actionable founder takeaways.

⚡ Your Fast-Track Cheat Sheet: Top 3 Takeaways from the Gold Box Pakistan Pitch

- Know your markup math cold — and own it. If your installment model charges 25%+ over base price, don’t hide behind euphemisms. Calculate your effective annualized rate, disclose it clearly, and be ready to defend why your target customer still benefits despite the cost. The sharks respect transparency far more than clever wording.

- Don’t ignore the Shariah conversation — engage with it strategically. In Pakistan, the interest question isn’t just a legal checkbox; it’s a brand-defining issue. Whether or not you pursue full Shariah compliance, understanding where your model sits on the spectrum — and having a roadmap for improvement — signals maturity to investors and builds trust with customers.

- The demand is real, but so is the risk. Millions of Pakistanis need installment-based purchasing options. Gold Box Pakistan proved the market exists. But reputational blowback, regulatory shifts, and default spikes can derail even a high-growth model. Build your business with buffers, legal foresight, and an ethical framework that can survive a shark’s toughest questions — because those questions don’t stop when the cameras turn off.