SME Funding in Pakistan 2026: All Government Schemes & How to Access Them

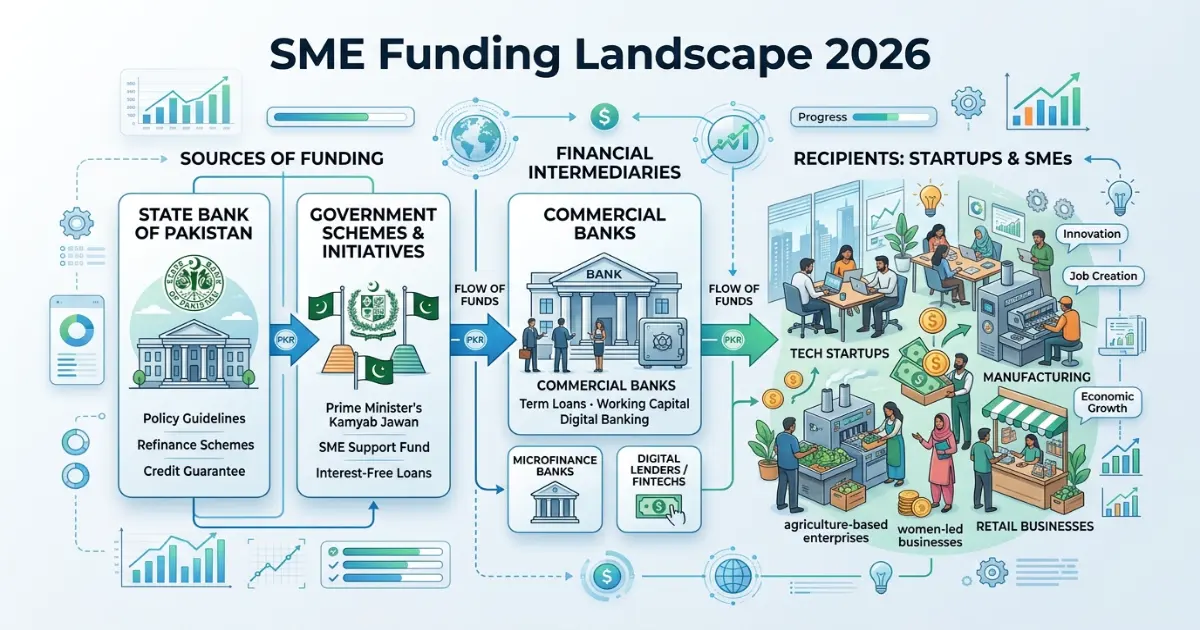

The most accessible SME funding in Pakistan for 2026 comes through the State Bank’s concessional refinance schemes and the PM’s Youth Business & Agriculture Loan (PMYBAL) — with mark-up rates as low as 0% for certain categories and loan sizes up to PKR 7.5 million under tiered Kamyab Jawan structures. But here’s what nobody tells you: the real bottleneck isn’t eligibility — it’s documentation readiness and bank-level friction. Knowing which scheme fits your stage, having a clean credit history, and walking in with a bank-ready file is what separates approved applicants from perpetual waitlists. This guide unpacks every active government SME funding window, how to apply, and how to avoid the five most common rejection traps.

If you’re running a small manufacturing unit in Gujranwala, a tech-enabled agri startup in Multan, or a women-led e-commerce brand out of your Karachi apartment — you’ve probably heard the same line from at least three bankers: “SME funding is available, sahib.” Then they hand you a form that might as well be written in hieroglyphics and ask for a NTN certificate you didn’t know you needed.

Here’s the truth: Pakistan’s government, through the State Bank of Pakistan (SBP), SMEDA, and provincial bodies, has pumped over PKR 500 billion into concessional SME financing lines in recent years. The schemes exist. The money is real. But between policy circulars, changing mark-up subsidies, and branch-level indifference, the average small business owner loses weeks just figuring out where to start.

This guide cuts through the noise. Whether you’re pre-revenue and need seed working capital, or you’re scaling a proven operation and need expansion funding, we’ll map every active scheme, show you how to decide which one fits, and walk you through the end-to-end application process — the way a practical mentor would, not a government PDF.

Why SME Funding in Pakistan Looks Different in 2026

Three things have reshaped the SME lending environment heading into 2026. First, the SBP’s phased exit from blanket subsidized refinance means several legacy schemes (like the Temporary Economic Refinance Facility) have wound down or merged, pushing banks to use their own balance sheets more — but with government credit guarantees covering a slice of the risk.

Second, the Kamyab Jawan program has been restructured and rebranded under the PMYBAL umbrella, with sharper focus on youth, women, and agriculture. Third, provincial governments — particularly Punjab and Sindh — have launched their own matching-grant and interest-free loan programs that don’t require navigating federal bureaucracy.

Translation: there’s more money than ever, but the pathways are more fragmented than they were in 2021-2023. If you’re applying blind, you’ll get lost. If you know exactly which scheme matches your profile, you can secure funding at effective rates that beat anything the private market offers.

All Active Government SME Funding Schemes in Pakistan (2026 Edition)

Let’s break down every scheme that’s actually open and disbursing funds right now. We’ll cover the loan size, mark-up rate, who qualifies, and the real-world catch with each one.

1. PM’s Youth Business & Agriculture Loan (PMYBAL) — Tiered Structure

This is the most widely marketed scheme and the one you’re most likely to hear about from a bank. It operates in three tiers, and the mark-up subsidy varies dramatically between them.

- Tier 1 (Up to PKR 0.5 million): 0% mark-up. Yes, zero. This is for nano-enterprises and first-time borrowers. Requires basic KYC, a simple business plan, and two guarantors. Available through select partner banks and NBP.

- Tier 2 (PKR 0.5M – 1.5M): 5% mark-up with the government subsidizing the rest. Requires slightly more documentation — bank statements, proof of business activity, and collateral or a personal guarantee depending on the bank’s internal policy.

- Tier 3 (PKR 1.5M – 7.5M): 7% mark-up (subsidized). Requires full documentation, including audited or accountant-certified financials, NTN, sales tax registration if applicable, and tangible collateral in most cases.

The catch: The 0% Tier 1 loans are politically popular but operationally slow. Banks aren’t incentivized to process tiny loans quickly. Expect 6 to 10 weeks from application to disbursement, and be prepared to follow up persistently.

2. SBP’s Refinance Scheme for Working Capital (RSWC)

Specifically for manufacturers and exporters who need working capital — raw material purchases, utility payments, inventory financing. Under this scheme, banks borrow from the SBP at a concessional rate and on-lend to SMEs at a capped spread. Current effective end-borrower rates hover around 7-9%, significantly below commercial lending rates of 16-20%.

- Loan size: Up to PKR 50 million for working capital needs

- Eligibility: Registered manufacturing or export-oriented SME with at least one year of operational history

- Key requirement: Must have a clean credit report from eCIB and an active current account with the lending bank for at least 6 months

3. SMEDA’s Credit Guarantee Scheme for Small Businesses

SMEDA doesn’t lend directly — but its credit guarantee scheme is arguably more valuable than a direct loan. Under this program, the government guarantees up to 40-60% of the loan amount, which dramatically reduces the bank’s risk and makes them far more willing to approve applications from SMEs that lack hard collateral.

- Coverage: Guarantees loans up to PKR 25 million

- Best for: Service-based businesses, tech startups, and women-led enterprises that may not own property to pledge

- Process: You apply through a partner bank; the bank evaluates your business, and if the only hurdle is insufficient collateral, they can invoke the SMEDA guarantee

4. Punjab Rozgar Scheme & Punjab Women Entrepreneurs Loan

The Punjab government, through the Punjab Small Industries Corporation (PSIC), runs targeted loan programs that are separate from federal schemes. In 2026, the Punjab Rozgar Scheme offers interest-free loans up to PKR 1 million for micro-enterprises, with a simplified application through designated branches of the Bank of Punjab. A parallel track for women entrepreneurs offers up to PKR 2 million at 3% mark-up.

5. Sindh Enterprise Development Fund (SEDF) — Matching Grants

Sindh’s approach is different: instead of subsidized loans, the SEDF offers matching grants of up to 30% of a project cost (capped at PKR 5 million) for enterprises in priority sectors like light engineering, food processing, and IT services. The grant is not a loan — you don’t repay it — but you must fund 70% of the project yourself or through a bank loan. This is ideal for expansion-stage SMEs that already have some liquidity.

6. KPK & Balochistan Micro-Enterprise Programs

Both provincial governments run small-scale programs through their respective small industries departments. KPK’s focus is on tourism-linked enterprises, handicrafts, and marble processing. Balochistan’s program — while smaller in scale — targets fisheries, date processing, and mining-adjacent SMEs. Loan ceilings are typically PKR 2-5 million with heavily subsidized rates.

7. EXIM Bank Export Refinance for SME Exporters

If you export — or plan to — EXIM Bank of Pakistan offers pre-shipment and post-shipment financing at rates benchmarked to LIBOR/SOFR plus a thin margin. For SME exporters shipping textiles, IT services, surgical goods, or agri-products, this is one of the cheapest sources of working capital available, often in the 5-7% range.

Comparison Table: Which SME Funding Scheme Fits Your Business?

| Scheme | Max Loan / Grant | Effective Rate | Best For | Collateral Required? |

|---|---|---|---|---|

| PMYBAL Tier 1 | PKR 0.5M | 0% | Nano startups, first-time borrowers | No (guarantors) |

| PMYBAL Tier 2 | PKR 1.5M | ~5% | Growing micro-enterprises | Sometimes (varies by bank) |

| PMYBAL Tier 3 | PKR 7.5M | ~7% | Established SMEs scaling up | Yes (typically) |

| SBP RSWC | PKR 50M | 7-9% | Manufacturers & exporters | Case-by-case |

| SMEDA Credit Guarantee | PKR 25M (guaranteed) | Varies (lower due to guarantee) | Collateral-light businesses | Partially (guarantee covers gap) |

| Punjab Rozgar | PKR 1M (interest-free) | 0% | Punjab-based micro-enterprises | Minimal |

| SEDF Matching Grant | PKR 5M (grant portion) | Grant (no repayment) | Sindh-based expansion projects | No (grant, not loan) |

| EXIM Export Refinance | Transaction-based | 5-7% | Active exporters | Export documents as security |

How to Access SME Funding in Pakistan: A Step-by-Step Action Plan

Step 1: Get Your Documentation House in Order (Before You Approach Any Bank)

This is where 60% of applications die. Walk into a bank without these, and you’ll be politely handed a checklist and shown the door. Here’s the minimum viable document stack for any SME loan application in Pakistan in 2026:

- Valid CNIC of all partners / directors

- NTN certificate (for the business and for each individual owner earning above the taxable threshold)

- Business registration document: Either SECP incorporation certificate (for private limited companies), partnership deed (for AOPs), or sole proprietorship declaration

- Sales tax registration (if applicable — required for loans above PKR 2M in most banks)

- Last 12 months of bank statements for the business’s current account

- Last 2 years of tax returns or accountant-certified financial statements

- Utility bills of the business premises (last 3 months)

- Proof of business activity: This could be purchase orders, invoices, supplier contracts, or an active lease agreement for your premises

Step 2: Choose the Right Scheme (Not the Most Generous One)

Many founders fixate on the scheme with the largest loan size or lowest mark-up. That’s backwards. Choose the scheme where you’re most likely to be approved, even if it’s smaller. A PKR 500,000 loan that lands in your account in 6 weeks is infinitely more useful than a PKR 5 million loan that sits in approval limbo for 8 months. Use the comparison table above to shortlist 2 schemes that match your stage, then apply to the one with the simpler documentation requirements first.

Step 3: Approach the Right Bank — Strategically

Not all banks are equally enthusiastic about SME lending. In practice, National Bank of Pakistan, Bank of Punjab, HBL, and Meezan Bank process the highest volumes of government-subsidized SME loans. But here’s a nuance: walk into the branch where you already hold your business current account. The relationship manager already knows your transaction history, which shortens the due diligence timeline. Cold-applying at a bank where you have no prior relationship adds weeks to the process.

Step 4: Prepare Your Business Plan (Even If They Don’t Ask)

For loans above PKR 1 million, banks will expect a basic business plan. It doesn’t need to be a 40-page MBA document. A clean 6-8 page plan covering what your business does, who your customers are, your last 12 months of revenue (real numbers), projected revenue for the next 12 months, and exactly how you’ll use the loan amount — that’s enough. Be specific about use of funds. “For business expansion” is vague and gets flagged. “PKR 800,000 for raw material procurement to fulfill a confirmed purchase order from XYZ Textiles dated March 2026” — that gets approved.

Step 5: Follow Up Without Being Annoying — But Be Relentless

Government-subsidized loans move slowly. Accept this. Check in with your relationship manager every 10-14 days. If you haven’t heard back in 4 weeks, escalate to the branch manager. If the branch drags its feet, contact the scheme’s designated helpline — PMYBAL has a dedicated portal, SMEDA has regional offices, and SBP’s Banking Services Corporation has a complaint resolution cell. Polite persistence is the game.

Which Route Should You Take? Adjusting Based on Your Business Stage

If You’re Pre-Revenue or Idea Stage…

You’re not eligible for most government SME loans — and that’s okay. Banks lend against cash flow history, not ideas. Your realistic options in 2026 are: (a) apply for a PMYBAL Tier 1 loan with a strong personal guarantor and a detailed project plan (some banks accept this for service-based startups with zero revenue if the plan is credible); (b) look into provincial micro-grant programs like the Punjab Rozgar Scheme’s startup track; or (c) pursue incubator-linked seed funding through NICs (National Incubation Centers) in Islamabad, Lahore, Peshawar, and Karachi, which often connect graduates to government-linked seed capital.

On Shark Tank Pakistan, we’ve seen several pre-revenue founders pivot to this exact hybrid approach — use the show for visibility, then leverage that visibility to access government programs that require “demonstrated traction.”

If You’re Generating Consistent Revenue (PKR 5M – 50M Annually)…

You’re in the sweet spot. The SBP’s RSWC and SMEDA guarantee schemes are designed precisely for you. Prioritize the SMEDA Credit Guarantee Scheme if you don’t own property — the guarantee coverage makes banks far more cooperative. If you’re exporting even PKR 2-3 million worth of goods per quarter, open an EXIM Bank conversation immediately. The rates are unmatched.

If You’re a Women-Led Business…

The State Bank mandates that 5% of all SME lending must go to women-led enterprises, and several schemes offer preferential terms. The Punjab Women Entrepreneurs Loan (2-3% mark-up) and the SBP’s women-entrepreneur refinance window are underutilized — meaning less competition for approvals. If you’re a woman founder, explicitly ask the bank about these quotas. Sometimes a branch manager doesn’t volunteer the information unless you ask.

If You’re in Agriculture or Agri-Tech…

PMYBAL’s agriculture track and Zarai Taraqiati Bank Limited (ZTBL) offer specialized crop and equipment loans. Additionally, the SBP’s “Asan Finance Scheme” for small farmers provides up to PKR 1 million with minimal paperwork. Agri-tech startups that blend tech with farming should look at hybrid paths — the SMEDA guarantee for the tech side, and ZTBL for the farming-operations side.

Common Mistakes That Get Your SME Loan Application Rejected — and How to Avoid Them

Mistake #1: Applying Before Your Documentation Is Ready

This is the #1 rejection reason across all schemes. Missing NTN, incomplete bank statements, or a business registration that doesn’t match the loan applicant’s name will get your file returned — and restarting takes weeks. Fix: Use the documentation checklist in Step 1 above. Have a trusted accountant review your file before you submit.

Mistake #2: Over-Leveraging Personal Guarantees

Some founders pledge personal assets (house, car) as collateral for a business loan without understanding the structure. If the business fails, those assets are at risk. Fix: Separate your personal and business liabilities. Use the SMEDA guarantee to reduce personal collateral exposure, and never pledge your primary residence for a loan under PKR 2 million — alternative schemes exist.

Mistake #3: Ignoring the Fine Print on Mark-Up Subsidies

Government-subsidized rates are contingent on timely repayment. Miss two installments, and the subsidy can be revoked — meaning your 7% loan could reset to the bank’s commercial rate of 18%+. Read the sanction letter carefully. Fix: Build a repayment buffer. If your monthly installment is PKR 45,000, keep PKR 90,000 liquid for at least the first three months.

Mistake #4: Applying to Multiple Banks Simultaneously Without Understanding Credit Inquiries

Every loan application generates a credit inquiry on your eCIB report. Three or four inquiries in a short window can make you look desperate to lenders and lower your credit score. Fix: Research first, shortlist one or two banks, and apply sequentially — not simultaneously.

Mistake #5: Believing “Interest-Free” Means Cost-Free

Even 0% mark-up loans carry processing fees, documentation charges, and insurance requirements that can add 1-3% to the effective cost. Fix: Ask the bank for a full cost schedule — not just the headline rate — before signing anything.

How to Use SharkTankPakistan.pk Tools to Strengthen Your Loan Application

One under-appreciated aspect of SME loan applications is valuation awareness. Even for a debt application (not equity), banks want to see that you understand what your business is worth and how the loan will improve its value. Our site offers free calculators that help you build that narrative:

- Startup Valuation Calculator: Run your numbers through our valuation tool to generate a defensible estimate of your business’s current worth. Include this in the “Business Overview” section of your loan application — it signals sophistication to the credit officer reviewing your file.

- Equity vs. Loan Calculator: If you’re debating between a government loan and an equity raise (perhaps through a Shark Tank Pakistan pitch), this tool shows you the long-term cost difference. For most stable SMEs earning 15-25% annual returns, a subsidized government loan is significantly cheaper than giving up equity.

Real-World Example: How a Lahore-Based Textile SME Secured PKR 3 Million Through SMEDA’s Guarantee

In early 2025, a small textile accessories manufacturer in Lahore’s Township Industrial Area — let’s call him Hamza — needed working capital to fulfill a bulk order from a Faisalabad-based exporter. His business had 3 years of consistent revenue (PKR 18-22M annually) but no hard collateral beyond machinery that was already depreciated on the books.

Hamza initially approached two commercial banks and was offered loans at 18% with a collateral demand he couldn’t meet. Through a SMEDA regional office referral, he learned about the Credit Guarantee Scheme. He applied through HBL, submitted his 2 years of tax returns, the purchase order from the exporter, and a simple 6-page business plan. SMEDA guaranteed 50% of the loan, the bank approved PKR 3 million at an effective rate of 8.5%, and the funds were disbursed in 9 weeks. The order was fulfilled. The loan is being repaid on schedule. The credit history he’s building now will make his next loan application — for PKR 8 million — dramatically smoother.

Lesson: Hamza’s story isn’t exceptional. It’s replicable. The SMEDA guarantee exists precisely for businesses like his. But he only found out about it because he visited the SMEDA office. Most SME owners never walk through that door.

When Government SME Funding Might NOT Be the Right Move

Government-backed loans aren’t always the best option. In some situations, they’re actually counterproductive:

- You need funds in under 3 weeks: Government scheme processing times will disappoint you. If speed is critical, a fintech lender or a high-interest bridge loan from a private NBFC (like FINCA or Khushhali Microfinance Bank) might serve you better — even at a higher rate — because the opportunity cost of waiting is greater.

- Your business is pre-revenue and the loan requires personal guarantees: Taking on personal debt for an unproven business model is exceptionally risky. Explore grants, incubator seed funding, or friends-and-family rounds first.

- You’re scaling fast and might raise equity soon: If you’re on a trajectory where you’ll likely pitch investors (or apply for Shark Tank Pakistan) within 12 months, taking on a large government loan could complicate your balance sheet and reduce your equity valuation. Run the equity-vs-loan calculator before committing.

- Your tax filings are incomplete or inconsistent: Applying for a government loan with messy tax records can trigger unwanted scrutiny. Clean your filings first, then apply.

Frequently Asked Questions About SME Funding in Pakistan

- Can I apply for a government SME loan without a registered business?

- It depends on the scheme. PMYBAL Tier 1 (up to PKR 0.5M) can be accessed with just a CNIC and a basic business plan — formal registration isn’t always required. But for loans above PKR 1M, banks will almost always demand SECP registration, partnership deed, or a sole proprietorship declaration along with NTN. If you’re serious about scaling, register your business before applying.

- How long does it take to get approved for PM’s Youth Business Loan in 2026?

- Realistically, 5 to 10 weeks from complete application submission to disbursement. Tier 1 loans (under PKR 0.5M) can sometimes process in 4-6 weeks if your documentation is flawless and the branch is actively processing. Larger Tier 3 loans can stretch to 12-14 weeks. Delays usually happen because of incomplete paperwork, not because the scheme is out of money.

- Are government SME loans available for tech startups or online businesses?

- Yes, but with caveats. Pure tech startups with no physical assets and inconsistent revenue are a harder fit for traditional bank lending. However, SMEDA’s Credit Guarantee Scheme and select provincial programs (especially in Punjab and Sindh) have expanded to include IT and IT-enabled services. If you have at least one year of revenue history and a current account with transaction volume, you have a viable path. Pre-revenue tech startups should look at incubator-linked seed funding instead.

- What is the maximum SME loan amount I can get from the government?

- Through the SBP’s Refinance Scheme for Working Capital, eligible manufacturing and export SMEs can access up to PKR 50 million. The PMYBAL program’s highest tier caps at PKR 7.5 million. For most small businesses, the practical ceiling is PKR 5-10 million unless you have substantial collateral, audited financials, and a multi-year track record.

- Do I need collateral for every government SME loan?

- Not for all. PMYBAL Tier 1 loans (up to PKR 0.5M) require only personal guarantors — no physical collateral. SMEDA’s Credit Guarantee Scheme covers 40-60% of the loan value, reducing the collateral burden. For larger loans (PKR 3M+), most banks will ask for some form of collateral — property, machinery, or a lien on inventory — but the SMEDA guarantee can cover the shortfall if you don’t have enough.

- Can women entrepreneurs access special SME funding rates?

- Yes. The SBP mandates that 5% of all bank SME lending goes to women-led businesses, and several schemes offer preferential rates. The Punjab Women Entrepreneurs Loan offers up to PKR 2 million at around 3% mark-up. Additionally, women applicants for PMYBAL are prioritized in the processing queue at several partner banks. Explicitly mention your eligibility for women-entrepreneur quotas when you apply.

- What happens if I miss a repayment on a government-subsidized SME loan?

- Missing even one or two installments can trigger the removal of the mark-up subsidy — meaning your concessional rate (say, 7%) could reset to the bank’s standard commercial rate (16-20%). Additionally, defaulted government-linked loans are reported to the eCIB, damaging your credit score and making future borrowing — from any bank — far more difficult. Always prioritize repayment over other expenses.

- Is Shark Tank Pakistan a better funding option than a government SME loan?

- They serve different purposes. Government loans are debt — you keep full ownership but must repay with interest (even if subsidized). Shark Tank Pakistan funding is typically equity-based — you give up a percentage of your business in exchange for capital and mentorship. For stable, cash-flow-positive SMEs, debt is usually cheaper long-term. For high-growth startups that need strategic guidance and industry connections, equity from a Shark might be more valuable than a loan. Use our Equity vs. Loan Calculator to model both scenarios before deciding.

🚀 Your Fast-Track Cheat Sheet: Top 3 Actions to Take This Week

- Audit your documentation. Pull together your CNIC, NTN, business registration, last 12 months of bank statements, and last 2 years of tax filings. If any of these are missing, make obtaining them your immediate priority. Without this stack, no application moves forward.

- Pick one scheme that matches your stage — not the biggest one. If you’re pre-revenue or nano-sized, target PMYBAL Tier 1 (0% mark-up, up to PKR 0.5M). If you’re generating consistent revenue, target the SMEDA Credit Guarantee Scheme or the SBP RSWC. Use the comparison table in this guide to lock in your choice.

- Walk into the bank where your business account already lives. Don’t cold-apply at a random branch. Your existing relationship manager can fast-track due diligence. Bring your documentation, your business plan, and a clear articulation of exactly how you’ll use and repay the funds. Follow up every 10 days until you have an answer.