PM Youth Business Loan Scheme 2026: The Complete Application Guide for Pakistani Startups

💡 The Quick Answer: The PM Youth Business Loan Scheme 2026 offers collateral-free, subsidized loans ranging from PKR 500,000 to PKR 7.5 million for Pakistani entrepreneurs aged 21 to 45. Interest rates are capped at 0% for the lowest tier and 5% for higher tiers, with repayment periods stretching up to 8 years. Applications are processed through designated partner banks — not through any third-party agent — and the scheme prioritizes first-time founders, women entrepreneurs, and applicants from underserved districts. The single most important thing to understand: this is a structured debt product, not a grant, not equity, and not a Shark Tank-style investment deal. You must repay every rupee, which makes your cash flow projections the most critical part of your application.

Let’s be honest about something most government loan guides won’t tell you upfront: getting approved for the PM Youth Business Loan 2026 is less about filling out a form correctly and more about proving you have a business that can actually generate enough cash to service the debt. Too many young Pakistani founders treat this scheme like a handout. The partner banks — National Bank of Pakistan, Bank of Punjab, Bank of Khyber, and others on the designated panel — treat it like a credit decision. That gap in understanding is why thousands of applications get rejected every year, and why this guide exists.

At SharksTankPakistan.pk, we spend our days analyzing how Pakistani startups get funded — whether through equity deals on Shark Tank Pakistan, angel investment, venture capital, or government-backed debt instruments like this one. The PM Youth Business Loan sits in a unique position: it is arguably the most accessible institutional funding source for early-stage Pakistani founders who don’t yet have the traction to attract private investors, but it comes with strings attached that equity funding simply does not. This guide will walk you through everything — eligibility, tiers, the application workflow, how banks actually evaluate your proposal, and where this loan fits (or doesn’t fit) alongside other funding options for Pakistani startups in 2026.

What Exactly Is the PM Youth Business Loan Scheme in 2026?

The Prime Minister’s Youth Business & Agriculture Loan Scheme (often shortened to PM Youth Business Loan) is a government-subsidized lending programme administered through the State Bank of Pakistan’s refinance framework and executed by designated commercial and specialized banks. It was launched to tackle one of the most persistent problems in Pakistan’s entrepreneurial ecosystem: young founders with viable ideas but zero collateral and no access to conventional bank credit.

In 2026, the scheme has matured through several iterations. The current version is markedly better than the original 2013 rollout — processing times are shorter, the application tracking system is partially digitized, and the tier structure now accounts for inflation-adjusted capital needs. But it is still, fundamentally, a government programme, which means paperwork, patience, and a willingness to navigate bureaucracy are prerequisites.

Here is what makes it genuinely valuable for Pakistani startups: no collateral is required for loans up to a certain threshold. The government partially guarantees the loan, absorbing some of the bank’s risk. This is not common in Pakistan’s commercial lending landscape, where most banks demand property, gold, or fixed deposits as security before even looking at your business plan. For a 24-year-old founder in Multan or Quetta with a solid idea and nowhere else to turn, that is a game-changer.

The Tier Structure in 2026

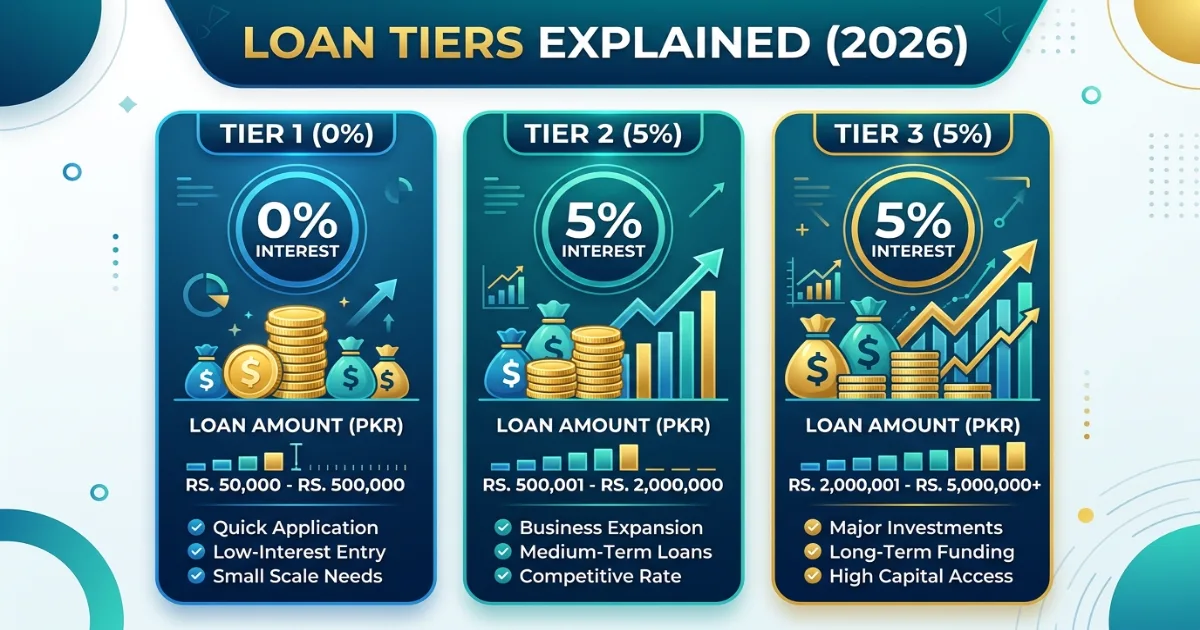

The scheme is divided into three tiers, and understanding which one you fall into shapes everything — from the interest rate you will pay to the documentation the bank expects.

| Tier | Loan Amount (PKR) | Interest Rate | Repayment Period | Collateral | Borrower Profile |

|---|---|---|---|---|---|

| Tier 1 | 500,000 – 1,500,000 | 0% | Up to 3 years | None | Micro-enterprises, home-based businesses, first-time founders |

| Tier 2 | 1,500,001 – 5,000,000 | 5% | Up to 5 years | None (partial govt guarantee) | Small enterprises, growing startups, service businesses |

| Tier 3 | 5,000,001 – 7,500,000 | 5% | Up to 8 years | Minimal / negotiable | Scaling businesses, manufacturing, agri-processing, tech-enabled SMEs |

A crucial detail that most generic articles gloss over: the 0% rate on Tier 1 is real, but the processing fees and bank charges can still add 1–2% in effective cost. Factor that into your calculations. Also, while Tier 2 and Tier 3 are listed at 5%, this is the end-borrower rate after the government subsidy — the actual commercial rate would be closer to 12–15% without the scheme. The subsidy is the reason these loans exist at all.

Who Can Actually Apply? Eligibility Beyond the Brochure

The official eligibility criteria are straightforward — Pakistani citizen, CNIC holder, aged 21 to 45, with a viable business plan. But the reality on the ground is more nuanced. Banks use additional filters that are not always published on the PM Youth Programme website. Based on conversations with loan officers and successful applicants, here is what actually matters:

- Age verification is strict. If you turn 46 before the loan is disbursed, your application may be voided even if you were 45 when you applied. Apply early in your eligibility window.

- CNIC must be valid and NADRA-verified. Expired CNICs or discrepancies between your CNIC address and your business location will trigger delays or rejections.

- Existing defaulters are automatically disqualified. If you have a past loan default reported to the eCIB (Electronic Credit Information Bureau), even if settled later, expect heightened scrutiny.

- Women and applicants from less-developed districts receive priority processing. This is a policy mandate, not just rhetoric. Banks have quotas they are expected to meet.

- You do not need a registered company at the time of application, but you will need to register your business (sole proprietorship, partnership, or private limited company) before the loan is disbursed. For Tier 3, a formally registered entity is almost always required.

PM Youth Business Loan vs. Shark Tank-Style Equity: A Real-World Comparison

One of the most common questions we receive at SharksTankPakistan.pk is whether founders should pursue a government loan or try to raise equity — either on Shark Tank Pakistan or from private investors. The answer depends on your business profile, your risk tolerance, and frankly, how much control you are willing to share. Here is how the two paths stack up in practical terms:

| Dimension | PM Youth Business Loan 2026 | Shark Tank Pakistan / Equity Funding |

|---|---|---|

| Cost of capital | 0–5% interest, plus ~1–2% in fees | Equity dilution (typically 15–40% per round) |

| Repayment obligation | Monthly instalments; must repay regardless of business performance | No repayment obligation; investors share the downside risk |

| Control retained | 100% ownership; bank has no say in business decisions | Reduced ownership; investors may demand board seats or veto rights |

| Approval speed | 4–12 weeks (varies by bank and tier) | 2–6 months (from pitch to term sheet to due diligence) |

| Mentorship / network | None; the bank is a creditor, not a partner | Potentially significant — Sharks bring expertise, connections, and credibility |

| Best for | Stable, cash-flow-positive businesses with predictable revenue | High-growth startups, scalable tech, businesses needing strategic guidance |

| Downside if things go wrong | Default ruins eCIB credit score; legal recovery action possible | Investors lose money; founder’s reputation affected but no personal debt liability (if structured as limited company) |

This comparison is not theoretical. We have seen Pakistani founders make the wrong choice — taking a loan for a pre-revenue app idea and drowning in repayments, or giving away 40% equity for a business that could have been funded with a cheap Tier 1 loan. The decision is critical, and it deserves more than a five-minute gut check.

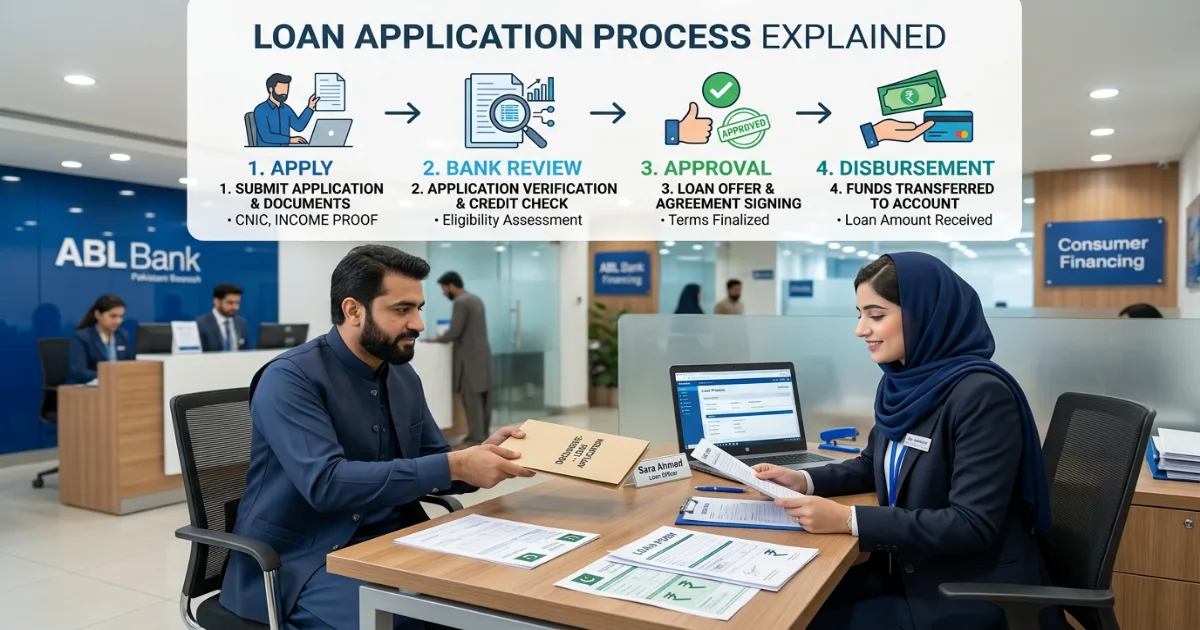

Step-by-Step: How to Apply for the PM Youth Business Loan in 2026

The application process has been streamlined compared to earlier years, but “streamlined” in the context of Pakistani government programmes still means multiple steps, physical visits, and patience. Here is the realistic workflow, not the sanitized version from the official brochure:

Step 1: Determine Your Tier and Prepare Your Business Plan

Before you approach any bank, decide which tier fits your capital need. Then build a business plan that speaks the bank’s language. This is not the same as a pitch deck for Shark Tank Pakistan. Banks care about three things: cash flow projections, the specific use of funds, and your personal financial history. Your business plan must include detailed monthly cash flow forecasts for at least the first two years, a clear breakdown of how every rupee of the loan will be spent, and evidence that your business can generate enough surplus to cover monthly instalments with a comfortable margin.

Step 2: Choose Your Partner Bank

The scheme operates through designated banks — primarily National Bank of Pakistan (NBP), Bank of Punjab (BoP), Bank of Khyber (BoK), Sindh Bank, and a rotating panel of others. Not all banks process all tiers equally. NBP handles the largest volume and has the most experience with the scheme, but also the longest queues. Bank of Punjab has been notably proactive with women-led business applications. Visit the branch, speak to the SME loan officer specifically (not the general customer service desk), and ask for the PM Youth Business Loan application kit.

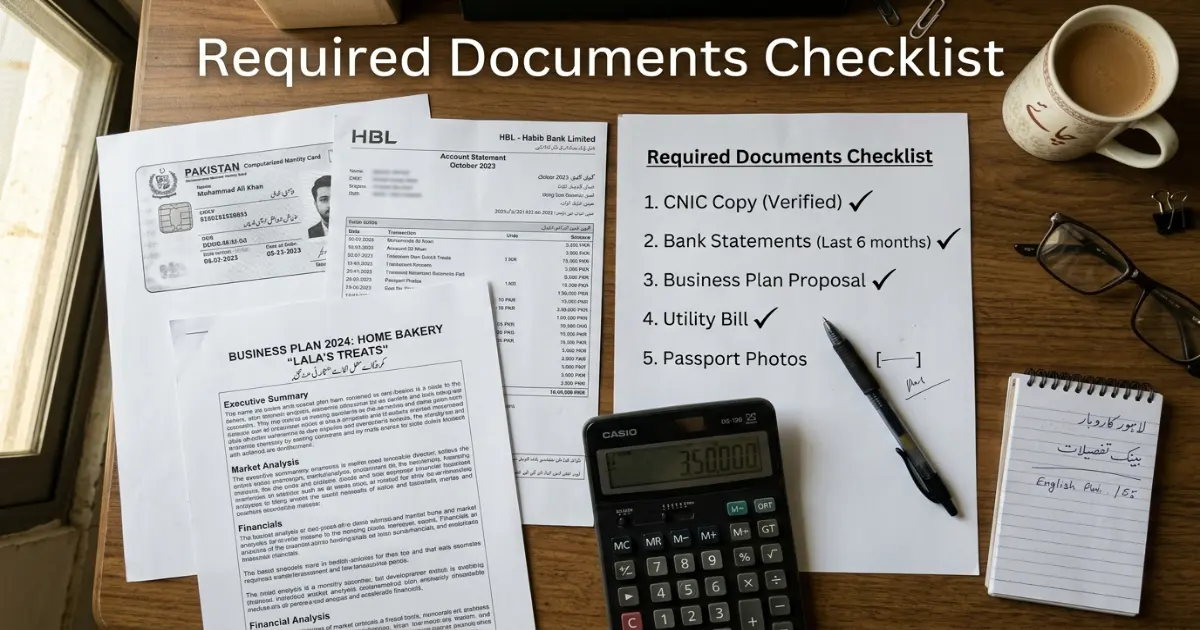

Step 3: Compile the Documentation

The document checklist typically includes: valid CNIC (original and copy), two passport-size photographs, proof of business address (rental agreement or utility bill), bank statements for the last 6–12 months (personal and business, if applicable), the detailed business plan, quotations for equipment or inventory you intend to purchase, any relevant licences or certifications (especially for food, health, or manufacturing businesses), and a personal guarantee undertaking. For Tier 3, audited financial statements or at least formally prepared accounts strengthen your case significantly.

Step 4: Submit and Follow Up — Diligently

Submit the complete dossier to the designated SME desk at your chosen bank branch. You will receive an acknowledgement receipt — keep this safe. The bank will conduct its own assessment, which may include a physical site visit to your business location. This visit is not a formality; loan officers are trained to assess whether the business exists in substance and whether the premises match the description in your application. After the assessment, the file goes to the bank’s credit committee. Approvals at this stage are discretionary — the scheme provides the framework and the subsidy, but the bank retains the final say on creditworthiness.

Step 5: Disbursement and Utilization Monitoring

Upon approval, the loan is disbursed — often in tranches tied to specific milestones or purchases. The bank may require invoices or receipts to release subsequent instalments. This is a utilization-check mechanism, and it is strictly enforced. If you said you would buy machinery and instead use the money for working capital, the bank can freeze the remaining disbursement. The first repayment instalment typically begins after a grace period of 3–6 months, depending on the nature of the business.

What Banks Really Look At (That Nobody Tells You)

Most rejection letters cite vague reasons like “business plan not viable” or “credit assessment unsatisfactory.” Here is what those phrases actually mean, decoded from conversations with loan officers and successful applicants across multiple banks:

- Debt Service Coverage Ratio (DSCR). This is the single most important number in your application. The bank calculates whether your projected monthly net income comfortably exceeds your projected monthly loan instalment. If the margin is thin — less than 1.3x or 1.5x coverage — expect a rejection. Build your projections conservatively, and ensure the DSCR is clearly visible in your business plan.

- Personal financial discipline. Your personal bank statements matter enormously. Frequent overdrafts, bounced cheques, or erratic cash movements raise red flags. The bank sees your personal financial behaviour as a proxy for how you will handle business finances.

- Business location and sector. Some sectors receive informal preference — agriculture, food processing, textiles, IT services. Others face informal headwinds — speculative real estate, unregulated trading, or businesses with high cash-in-hand components that are difficult to document.

- Guarantor strength. For Tier 2 and Tier 3 loans, having a guarantor with a stable income and clean credit history can be the deciding factor. This person is not providing collateral, but they are legally co-signing the debt.

Situation-Based Guidance: How the Advice Changes for Different Founders

Not all applicants are starting from the same place. Here is how your strategy should shift based on your specific situation:

If You Are Pre-Revenue (No Sales Yet)

Your application will face intense scrutiny. Banks are not venture capitalists; they are uncomfortable funding ideas. Your best move is to apply for Tier 1 only, focus your business plan on a product or service with demonstrated local demand (cite market surveys, competitor analysis, or even pre-orders), and emphasize that the loan will be used for tangible, resellable assets — not for salaries or marketing. A pre-revenue SaaS startup is a poor fit. A pre-revenue bakery with a rented location, equipment quotations, and 50 customer pre-orders is a much stronger candidate.

If You Are Already Generating Revenue

Your existing cash flow is your strongest asset. Include bank statements that prove consistent revenue, highlight repeat customers, and present the loan as expansion capital — not survival capital. Banks love lending to businesses that don’t strictly need the loan but can use it to grow faster. Frame your application around scaling something that is already working.

If You Are a Woman Founder

The scheme has explicit provisions for women entrepreneurs, including a mandatory quota for banks. Some banks — particularly Bank of Punjab — have dedicated women’s entrepreneurship desks. Use this to your advantage by specifically requesting the women’s business loan officer when you visit the branch. Your application will still be assessed on merit, but the processing priority and the institutional willingness to engage are tangibly better.

If You Are Considering Both This Loan and Shark Tank Pakistan

Think carefully about sequencing. Taking a government loan first and then appearing on Shark Tank Pakistan with existing debt on your books is not inherently disqualifying — but it changes the equity conversation. A Shark will factor your debt obligations into their valuation, and the monthly repayments reduce the free cash flow that makes your business attractive. If your business is debt-friendly (asset-heavy, predictable revenue), take the loan. If it is equity-friendly (scalable, high-growth, currently unprofitable), pursue Shark Tank Pakistan or angel investment first and only consider the loan later, once your revenue is stable enough to service it.

Common Pitfalls & When NOT to Apply for This Loan

This section is as important as everything above. The PM Youth Business Loan is a valuable tool, but it is the wrong tool for many situations. Here are the most frequent mistakes — and the scenarios where you should genuinely reconsider applying:

- Borrowing the maximum just because you can. Many founders see “up to PKR 7.5 million” and immediately aim for the top. That is dangerous. Every rupee borrowed must be repaid with interest (even at 5%, that compounds). If your business can achieve its next milestone with PKR 2 million, do not borrow PKR 5 million. Excess debt kills more startups than underfunding does.

- Using the loan for personal expenses. This sounds obvious, but it happens more often than anyone admits. Loan utilization is monitored, and misusing funds is a fast track to default and legal trouble.

- Underestimating the time commitment. The application process is not a one-week endeavour. Expect 4–12 weeks from first visit to disbursement, and plan your business timeline accordingly. If you need capital urgently — within a week — this scheme is not the right vehicle.

- Applying without a proper business plan. A five-page document downloaded from the internet and filled in half-heartedly will not pass. The bank’s SME officer has seen hundreds of those. Your business plan needs to be specific, locally grounded, and financially rigorous.

- When NOT to apply: If your business is purely speculative (e.g., cryptocurrency trading, unregulated investment schemes). If you have an existing default or poor eCIB history that you have not resolved. If your business model cannot demonstrate a clear path to consistent monthly cash flow. If you are not prepared for the psychological weight of debt — because unlike equity, debt does not sleep, does not forgive, and does not share your optimism about the future.

How to Use SharkTankPakistan.pk Tools Alongside Your Loan Application

While the PM Youth Business Loan is processed through banks and not through any platform like Shark Tank Pakistan, several of the calculators and resources on SharksTankPakistan.pk can directly improve the quality of your loan application:

- Equity & Loan Calculator: Before you commit to a loan amount, use our equity and loan calculator to model what your monthly repayments will look like at different borrowing levels. This is the same DSCR thinking that banks apply — get ahead of it.

- Startup Valuation Calculator: If you are weighing a loan against potential equity investment, run your business through the startup valuation calculator to understand what percentage of your company you would need to give away to raise the same amount of capital. The comparison often makes the 5% loan look remarkably attractive.

- Shark Tank Pakistan Pitch Analysis: Read through our breakdown of the best pitches from the show. The financial clarity that impresses Sharks — knowing your numbers cold, understanding your unit economics, projecting realistically — is exactly the same clarity that impresses a bank loan officer. The audience is different; the rigour is identical.

Real-World Snapshot: A Pakistani Startup That Got It Right

Consider the case of a small food processing unit in Faisalabad — let’s call the founder Ahmed. He was 29, with two years of experience running a home-based freeze-dried fruit business that was generating about PKR 150,000 in monthly revenue. He needed PKR 3 million to lease a small commercial processing facility and buy a freeze-drying machine. He applied for a Tier 2 PM Youth Business Loan through Bank of Punjab.

Ahmed’s application succeeded for three reasons: first, his business was already generating revenue, so the bank could see real cash flow, not just projections. Second, he provided three formal quotations for the machinery, showing he had done his procurement homework. Third, his business plan included a detailed monthly cash flow forecast that explicitly showed a DSCR of 1.9x — meaning his projected net income was nearly double the loan instalment. The loan was approved in seven weeks, and two years later, his business has scaled to PKR 700,000 in monthly revenue with a full-time staff of eight.

Ahmed could have tried Shark Tank Pakistan instead. But his business — while solid — was not “venture scale.” It was never going to 10x in three years. For that profile, a subsidized loan was the smarter route than giving away equity for a growth trajectory that was never realistic. This is the kind of clear-eyed self-assessment that separates successful applicants from those who waste months pursuing the wrong funding path.

Frequently Asked Questions About the PM Youth Business Loan 2026

What is the maximum loan amount under PM Youth Business Loan 2026?

The maximum loan amount is PKR 7.5 million under Tier 3 of the scheme. This tier is designed for scaling businesses and typically requires a formally registered business entity, a detailed business plan, and in some cases a guarantor. Interest is capped at 5% with a repayment period of up to 8 years.

Is the PM Youth Business Loan really interest-free for small amounts?

Yes, Tier 1 loans (PKR 500,000 to PKR 1,500,000) carry a 0% interest rate. However, applicants should budget for processing fees and bank charges that typically add 1–2% in effective cost. The interest subsidy is funded by the government through the State Bank of Pakistan’s refinance mechanism.

Can I apply for the PM Youth Business Loan if I don’t have a registered company yet?

You can apply without a registered company, but you must complete business registration — whether as a sole proprietorship, partnership, or private limited company — before the loan is disbursed. For Tier 3 loans, a formally registered entity is almost always required by the partner bank.

How long does the PM Youth Business Loan application process take in 2026?

Expect 4 to 12 weeks from the date you submit a complete application to disbursement. Processing speed varies significantly by bank, tier, and the completeness of your documentation. Incomplete applications are the single biggest cause of delays. NBP typically processes the highest volume and may take longer than smaller partner banks.

Do I need collateral for the PM Youth Business Loan?

Tier 1 loans require no collateral. Tier 2 loans are also collateral-free under the government’s partial guarantee framework. Tier 3 loans may require minimal or negotiable security depending on the bank’s internal credit assessment. A personal guarantee (not asset-backed collateral) is standard across all tiers.

Can women entrepreneurs apply for the PM Youth Business Loan?

Yes, and women-led businesses receive priority processing under the scheme’s explicit policy mandates. Several partner banks — notably Bank of Punjab — have dedicated women’s entrepreneurship desks. The eligibility criteria, interest rates, and loan limits are identical, but the institutional support and processing speed tend to be better for women applicants.

What happens if I default on a PM Youth Business Loan?

Defaulting has serious consequences. Your name is reported to the eCIB (Electronic Credit Information Bureau), which will severely damage your credit score and make future borrowing — personal or business — extremely difficult. The bank can initiate legal recovery proceedings, and the government guarantee does not protect the borrower from liability. Treat this as a real debt obligation.

Is the PM Youth Business Loan better than getting equity investment from Shark Tank Pakistan?

It depends entirely on your business model. The loan is cheaper capital (0–5% vs giving up 15–40% equity), but it must be repaid regardless of business performance. Equity is more expensive long-term but shares the downside risk. Stable, cash-flow-positive businesses lean toward loans. High-growth, pre-revenue, or tech-centric startups often find equity more suitable despite the dilution.

🚀 Your Fast-Track Cheat Sheet: Top 3 Actions to Take

- Run the numbers before you apply. Use the SharksTankPakistan.pk Equity & Loan Calculator to model your monthly repayments at different borrowing levels. If your projected DSCR is below 1.5x, either reduce the loan amount or strengthen your revenue model. Banks will do this same math — beat them to it.

- Match your funding type to your business DNA. Asset-heavy, cash-flow-stable businesses (food, manufacturing, retail, agri-processing) are strong candidates for this loan. Pre-revenue tech startups, speculative ventures, and businesses with unpredictable income should seriously consider equity funding through Shark Tank Pakistan or angel investors instead. The wrong funding choice can sink an otherwise viable business.

- Prepare your documentation with bank-level rigour. A detailed, locally grounded business plan with clear cash flow projections, formal equipment quotations, and clean personal bank statements is non-negotiable. Visit the branch, speak to the SME loan officer directly, and treat the application process with the same seriousness you would bring to a Shark Tank Pakistan pitch. The bank is not an investor — but it is the gatekeeper to the most accessible institutional capital available to young Pakistani founders in 2026.